Toyota's Captive Faces CFPB, DOJ Enforcement Action

Toyota Motor Credit Corp. revealed in a regulatory filing that it could face an enforcement action from the Consumer Financial Protection Bureau and the U.S. Department of Justice.

Toyota Motor Credit Corp. revealed in a regulatory filing that it could face an enforcement action from the Consumer Financial Protection Bureau and the U.S. Department of Justice. According to the November 28 filing with the Securities and Exchange Commission (SEC), the two agencies allege that the captive’s practices have resulted in discriminatory pricing of loans, according to F&I and Showroom magazine.

In an emailed statement to F&I and Showroom Monday, Toyota’s finance arm said that over the past two and a half years, it has “has activated a stronger, more robust Compliance Management System (CMS)” to help realize its consumer protection and regulatory compliance goals. It also noted that it does not collect consumer data related to race or ethnicity.

“Our intent is that these measures will contribute to a solution that meets the CFPB’s expectations and allows us to better serve our customers,” the statement read, in part. “In the meantime, and in keeping with our commitment to fair and responsible lending practices, it is important for our customers to know that we do not track the race or ethnicity of our customers or credit applicants, and these factors never influence our credit or pricing decisions.”

The captive said in its filing that it was notified of the potential enforcement action in a November 25 letter issued by the CFPB and DOJ. This notice comes a little more than a year since the captive revealed in a September 2013 filing that the bureau and the DOJ requested information regarding its pricing practices for loans it funds through auto dealers.

The finance source, which Experian Automotive had as the No. 3 finance source in the third quarter with a 4.49-percent share of the market, said in its recent SEC filing that it intends to cooperate with the agencies’ investigation.

“… We received from the agencies a letter alleging that such practices resulted in discriminatory pricing of loans to certain borrowers in contravention of applicable laws, and informing us that they are prepared to initiate an enforcement proceeding unless we agree to a voluntary resolution satisfactory to them,” the filing read, in part. “The agencies have indicated that they are seeking monetary relief and implementation of changes to our discretionary pricing practices and policies, which … could adversely affect our business.”

Nearly a year ago, the CFPB and DOJ took action against Ally Financial over similar allegations: The finance source was fined $98 million for allegedly engaging in an “ongoing nationwide pattern or practice of discrimination” against African-American, Hispanic and Asian/Pacific Islander borrowers in its auto lending since April 1, 2011.

Starting with a bulletin it issued in March 2013, the CFPB has said lenders will be held responsible for unlawful, discriminatory pricing that is the result of policies that allow dealers to mark up the interest rate on an auto loan in exchange for services rendered. A recent report by the American Financial Services Association, however, found that the bureau’s methodology for determining the presence of discriminatory in auto lending is inherently flawed.

The CFPB declined to comment on the action against Toyota Motor Credit when contacted by F&I and Showroom.

More Operations

Manheim Index Shows Used-Vehicle Wholesale Prices Up 2.1% in June

The market is seeing stronger appreciation in older used vehicles this year, and the most affordable segments have been among the year’s best performers.

Read More →

Commercial Fleet Sales Contribute To June, YTD Gains

The fleet sector has boosted its vehicle purchases at a reliable pace in the first half of this year compared with 1H 2025.

Read More →

Stop Remarketing Electric Vehicles Like Gas Cars

The advantages and attributes of electric vehicles are upending the traditional remarketing cycle, requiring fleet sellers to rely on new factors and approaches detailed below.

Read More →

AP Fleet Management Expands Remarketing Program for Commercial Work Trucks

AP Fleet Management expanded its commercial vehicle remarketing program with dedicated resale services and an online marketplace for used work trucks.

Read More →

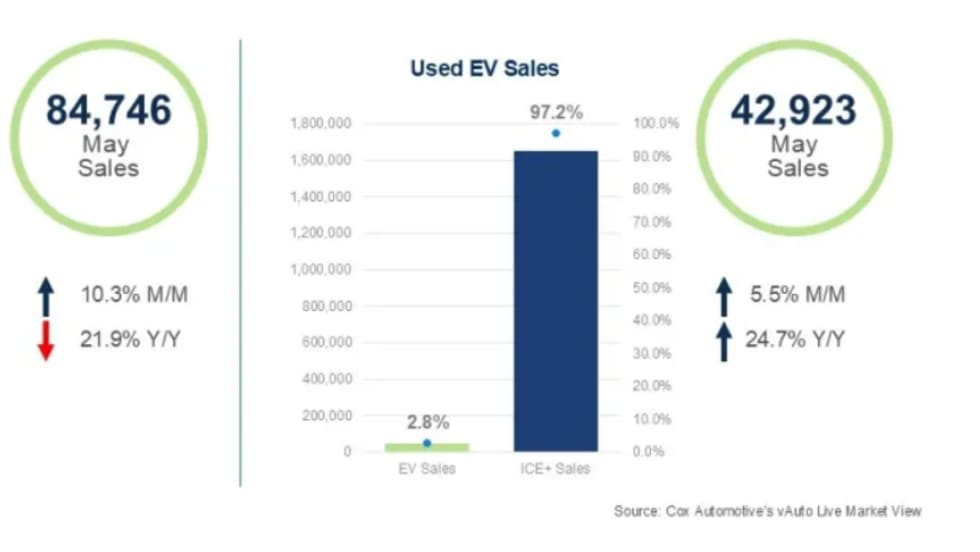

Used EVs Strengthen Overall Electric Vehicle Market

The latest sales data point to several reasons for the divergent trends in new and used EVs that can factor into fleet cycling decisions.

Read More →

The Data-Driven Haul: 5 Ways AI is Leveling the Playing Field in Auto Transport

Large and small transport fleets are becoming more competitive as predictive analytics and real-time data inform the logistics decision chain.

Read More →

2026 CAR Awards Celebrate Industry Excellence

CAR’s annual Fleet Remarketing Awards opened a reimagined 2026 conference designed to bridge the worlds of fleet management and automotive remarketing.

Read More →

CAR 2026 Recap Part 2: Closing the Gap Between Data & Remarketing Value

The second half of CAR 2026 examined how fleets can translate lifecycle strategy, vehicle data, and market shifts into higher real-world results.

Read More →

CAR2026 in Two Words: Velocity, Value (Part 1)

The 2026 Conference of Automotive Remarketing convened with a mandate to involve a new constituency — fleet managers — and an updated mission to demonstrate unrealized value in de-fleeted vehicles.

Read More →

CAR 2026: Get the Wall Street Update on the Key Players in Remarketing

From a Wall Street analyst's take on remarketing's key players to whether fleets need their own version of Carfax, CAR 2026's afternoon roundtables will answer key operational and industry questions.

Read More →