Related News:Used Vehicles Inventory Mostly Flat As Sales Slow

Tariffs Not Raising New Vehicle Prices So Far

Enough vehicles are sitting on lots as vehicle days’ supply hovers above last year’s levels, and sales volume lingers well below available inventory.

July 11, 2025

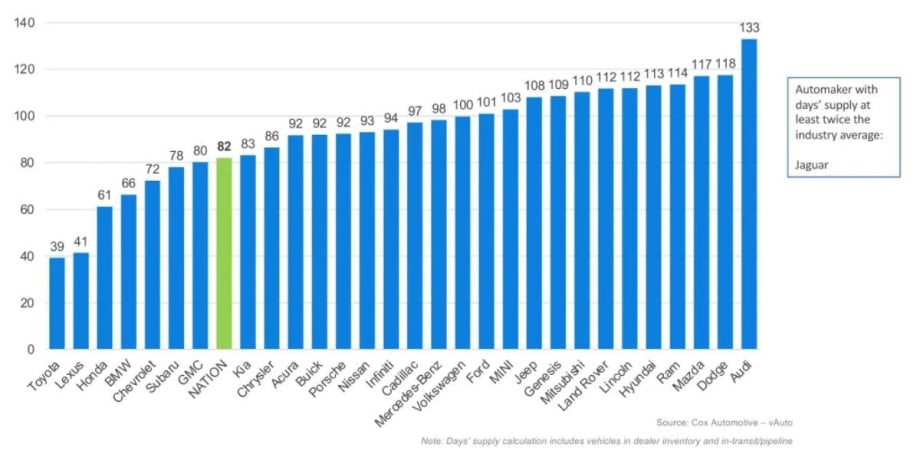

New-vehicle days’ supply reached 82 at the start of July, 12 days higher than the month-earlier measure.

Graphic: Cox Automotive

3 min to read

Everyone is hunting for clear evidence of higher prices on new vehicles driven by tariffs, yet the story hasn’t materialized.

Automakers continue to resist raising the manufacturer’s suggested retail prices (MSRPs) as demand remains tepid and policy has yet to solidify.

Vehicle Inventory Up

New-vehicle inventory has started to grow as next-model-year vehicles (MY2026) appear on dealer lots. However, the volume of these vehicles is still down more than 20% from last year, according to the Cox Automotive analysis of vAuto Live Market View data released July 10.

July opened with 2.83 million new vehicles available on dealer lots across the U.S., representing a 14.5% increase from 2.47 million units measured at the beginning of June, but still 1.4% lower than last year. The supply increase was generally observed across all automakers, with none significantly contributing to the overall rise. Despite this, sales have not kept pace with the increased supply, resulting in new-vehicle days’ supply reaching 82 at the start of July, which is 12 days higher than the month-earlier measure.

Cox Automotive’s vAuto Live Market View days’ supply is based on the estimated daily retail sales pace for the most recent 30-day period. The 30-day sales pace measured at the end of June was mostly flat compared to the previous month — up about 0.5% month over month — but is notably lower than the pace in April and May. Year over year, the June sales pace rose 2.2% from June 2024.

Next-model-year inventory has increased to over 7% of the total, a jump of 95% month-over-month, but is still about 21% lower than what was reported at the same time last year. As tariffs particularly impact luxury makes from Europe, a careful look at those brands suggests BMW continues to differ from its German compatriots in growing its MY 2026 vehicle inventory to over a third of available inventory, while Mercedes-Benz shows under 2% and Audi shows none. The latter two are likely carefully managing shipments of tariffed vehicles.

However, when reviewing the mix of models being replenished on showroom floors, imports of some of the most affordable products seem to have been mostly uninterrupted despite tariff challenges. Some of the biggest increases in stock have been in volume models coming out of South Korea, such as the Buick Encore GX, Chevrolet Trax, and Chevrolet Trailblazer, as well as from Mexico, including the Chevrolet Equinox, Ford Maverick, and Honda HR-V.

New-Vehicle Listing Prices Flat in June

The average new vehicle listing price at the end of June remained flat month over month, down by only $84 to $48,749. Compared to last year, average listing prices were 3.1% higher. Nearly every automaker’s average listing price swung less than 2% higher or lower than the previous month. Interestingly, with new model year inventory, both BMW and Mercedes-Benz show a month-over-month decrease in average listing price. At the same time, Audi has increased despite holding back on the fresher metal.

According to Kelley Blue Book, a new vehicle’s average transaction price (ATP) was $48,907 in June, representing a month-over-month increase of $108. In other words, flat. New-vehicle sales incentives are mainly steady, increasing month over month in June by just 0.1 percentage point to 6.9% of ATP. [The full ATP report will be published on July 14.]

As inventory levels rise and new model year vehicles populate dealer lots, the automotive market finds itself in a delicate balance. Demand has not matched supply growth, pushing days’ supply higher, and average listing prices have mostly plateaued.

With incentives holding relatively firm as well, shoppers can expect a market marked by incremental change rather than dramatic shifts. Tariff negotiations have been kicked down the road for another three weeks, which means it could be the fourth quarter before any sizable increase in overall consumer prices.

For now, patience remains a virtue, and attentive consumers may find value by tracking nuanced movements in pricing and inventory as the year progresses.

Originally posted on Automotive Fleet

More Fleet

Commercial Fleet Sales Contribute To June, YTD Gains

The fleet sector has boosted its vehicle purchases at a reliable pace in the first half of this year compared with 1H 2025.

Read More →

Registration Opens for 2026 Fleet Forward Conference

Held on the East Coast for the first time, the Washington, D.C.-area event features expert-led education, a new IIHS Crash Test Experience, and collocation with the NAFA’s Fleet Safety Symposium.

Read More →

AP Fleet Management Expands Remarketing Program for Commercial Work Trucks

AP Fleet Management expanded its commercial vehicle remarketing program with dedicated resale services and an online marketplace for used work trucks.

Read More →

Used EVs Strengthen Overall Electric Vehicle Market

The latest sales data point to several reasons for the divergent trends in new and used EVs that can factor into fleet cycling decisions.

Read More →

Wholesale Used Vehicle Market Sustains Moderate Rise In Values, Prices

Trends continue to normalize after a strong start to the year, as consumers contend with higher gas prices in the coming summer months.

Read More →

Commercial Fleet Sales Still Lead Sectors Despite May Mini Dip

The U.S. economy's continued growth and positive business investment are creating a favorable environment for fleet vehicle demand.

Read More →

The Data-Driven Haul: 5 Ways AI is Leveling the Playing Field in Auto Transport

Large and small transport fleets are becoming more competitive as predictive analytics and real-time data inform the logistics decision chain.

Read More →

Commercial Fleet Sales Show Healthy Gains

So far, the fleet sector is outshining government and rental fleet sales this year as economic growth spurs more business investment.

Read More →

CAR 2026 Recap Part 2: Closing the Gap Between Data & Remarketing Value

The second half of CAR 2026 examined how fleets can translate lifecycle strategy, vehicle data, and market shifts into higher real-world results.

Read More →

CAR2026 in Two Words: Velocity, Value (Part 1)

The 2026 Conference of Automotive Remarketing convened with a mandate to involve a new constituency — fleet managers — and an updated mission to demonstrate unrealized value in de-fleeted vehicles.

Read More →