Rising Wholesale Vehicle Volumes Pressure Auto Transport System

New-Vehicle Production and Sales Steady as Supply Declines

The average listing price of a vehicle remained above $47,000 since April, while the ATP of a new vehicle in July was $48,334 compared with $48,671 in June.

August 14, 2023

After robust sales in June and July, Honda had the lowest new-vehicle inventory among all brands. Toyota, Kia and Subaru also had low supply, as did Lexus, Land Rover and Cadillac and Lexus among luxury brands.

Graphic: Cox Automotive

4 min to read

New-vehicle inventory at the end of July was mostly unchanged from the end of June, as production and sales remained generally balanced through the month, according to Cox Automotive’s analysis of vAuto Available Inventory data released on Aug 10.

The total U.S. supply of available unsold new vehicles stood at 1.96 million units at the end of July, down just slightly from a revised 1.98 million at the start of the month. Inventory numbers include vehicles available on dealer lots and some in transit. Supply was up 71% from a year ago, or more than 800,000 units higher, about the same as the month earlier.

Days of supply stood at 56 at the end of July, unchanged from a revised 56 at the start of the month. That was 39% higher than the same time a year ago. Historically, 60 days’ supply across the industry was considered normal and ideal. While inventory has rebounded from 2021 and 2022 levels, it remains low by historical standards.

The Cox Automotive days’ supply is based on the daily sales rate for the most recent 30-day period. Sales are up 24% from a year ago. For the full calendar month of July, total new-vehicle sales rose 15% over the previous year on top of a 23% increase in June. The seasonally adjusted annual rate (SAAR) in June and July was 15.7 million. The strength in July sales was again supported by strong sales growth to fleets, up 35% year-to-year.

New-Vehicle Prices Open August Above $47,000

The average listing price – or asking price – remained above $47,000, where it has been since April. As August opened, the average listing price was $47,048, down slightly from where the month started at $47,162. The average listing price was down 0.9% year over year.

In July, the average transaction price (ATP) – the price paid – rose a scant 0.4% from a year ago, the smallest year-over-year price increase in the last decade. The ATP of a new vehicle in July was $48,334, compared with $48,671 in June, according to Kelley Blue Book. Since the start of the year, transaction prices are down 2.7%, or $1,335, the largest January to July fall in the past decade.

Incentives increased for the tenth consecutive month in July to the highest level since October 2021, averaging $2,148 per vehicle, or 4.4% of the ATP. A year ago, incentives were only 2.4% of ATP. As inventories improve, discounts and incentives are expected to increase.

Electric Vehicle Inventory Remains Well Above Industry Average

The inventory of new EVs, as measured by days’ supply, fell slightly in July, dropping to 100 days from 103 days in June. The days’ supply numbers exclude Tesla and Rivian, which sell direct to consumers and do not carry dealer stock. Only ultra-luxury vehicles and high-end luxury cars had more inventory.

Among the best-selling EVs, the Chevy Bolt – one of the most affordable EVs available – had the lowest days’ supply, at less than 35 days. The BMW i4 also had a relatively low days’ supply at the end of July, as did the Cadillac Lyriq, which has been slow to ramp up.

On the other end of the spectrum, many EVs had more than 100 days’ supply, indicating that EV availability is rapidly increasing as automakers improve production capabilities. EVs from Hyundai, Kia and Nissan all have 100+ days’ supply. Days’ supply of the Ford F-150 Lightning in July was 74, lower than the non-EV version of the F-150. Mustang Mach-E days’ supply was higher.

The higher days’ supply is not necessarily an indication of weak demand but an expected part of EV growth as automakers ramp up production and expand offerings. Higher inventory levels are pressing EV prices down, which can increase sales. In July, the average transaction price paid for a new EV was nearly 20% lower than it was one year ago when EV prices peaked. The lower prices last month were mostly driven by significant price cuts at Tesla and an increase in Chevy Bolt sales compared to one year ago.

Inventory Varies by Brand and Price Points

Import non-luxury and luxury brands had the lowest inventories in July. The highest inventories for non-luxury brands were dominated by Stellantis’ brands and a mix of foreign and domestic luxury makes.

After robust sales in June and July, Honda had the lowest new-vehicle inventory among all brands. Toyota, Kia and Subaru also had low supply, as did Lexus, Land Rover and Cadillac and Lexus among luxury brands.

Luxury brands Infiniti and Buick had the highest inventory, with more than 80 days’ supply. Non-luxury brands with the highest inventory were Stellantis brands – Ram, Jeep, Chrysler and Dodge, with more than 100 days’ supply.

As has been the case for months, the higher price brackets had the beefiest supplies. The $50,000 to $60,000 segment had the heftiest inventory, with 79 days’ supply. At the opposite end of the price spectrum, vehicles under $20,000 had the least with 28 days’ supply.

More Fleet

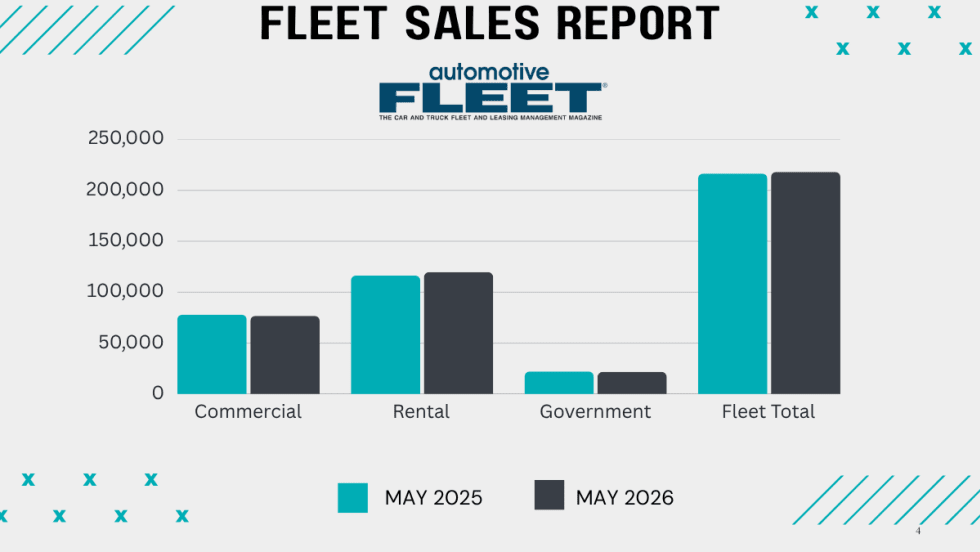

Commercial Fleet Sales Contribute To June, YTD Gains

The fleet sector has boosted its vehicle purchases at a reliable pace in the first half of this year compared with 1H 2025.

Read More →

Registration Opens for 2026 Fleet Forward Conference

Held on the East Coast for the first time, the Washington, D.C.-area event features expert-led education, a new IIHS Crash Test Experience, and collocation with the NAFA’s Fleet Safety Symposium.

Read More →

AP Fleet Management Expands Remarketing Program for Commercial Work Trucks

AP Fleet Management expanded its commercial vehicle remarketing program with dedicated resale services and an online marketplace for used work trucks.

Read More →

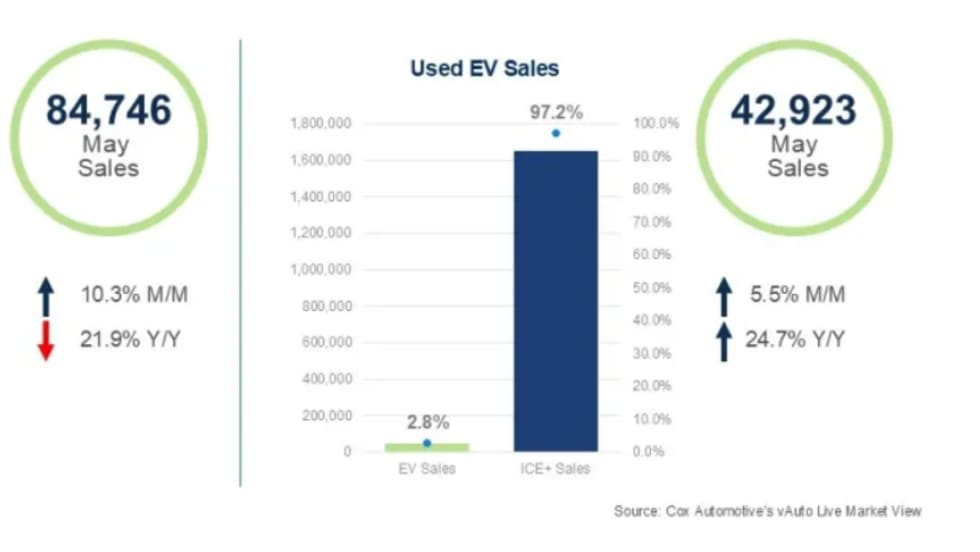

Used EVs Strengthen Overall Electric Vehicle Market

The latest sales data point to several reasons for the divergent trends in new and used EVs that can factor into fleet cycling decisions.

Read More →

Wholesale Used Vehicle Market Sustains Moderate Rise In Values, Prices

Trends continue to normalize after a strong start to the year, as consumers contend with higher gas prices in the coming summer months.

Read More →

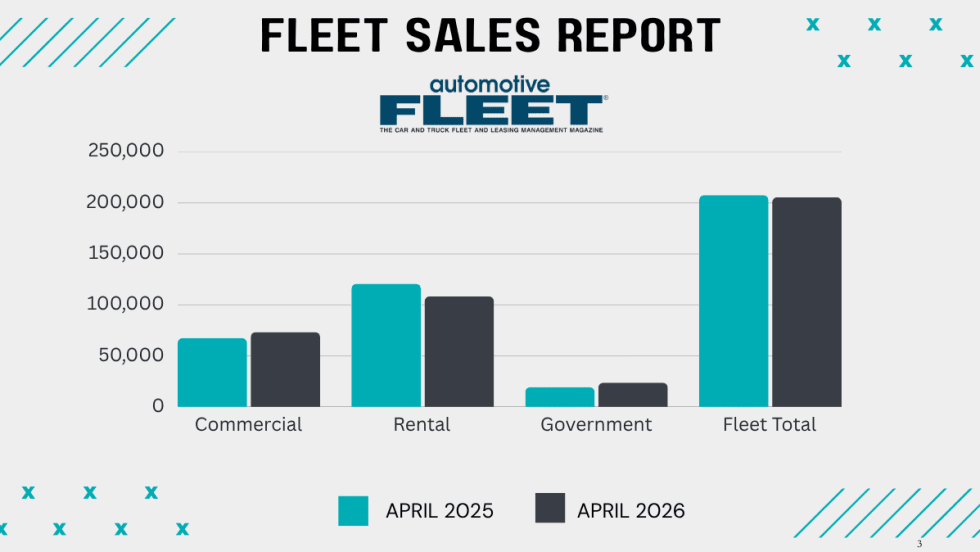

Commercial Fleet Sales Still Lead Sectors Despite May Mini Dip

The U.S. economy's continued growth and positive business investment are creating a favorable environment for fleet vehicle demand.

Read More →

The Data-Driven Haul: 5 Ways AI is Leveling the Playing Field in Auto Transport

Large and small transport fleets are becoming more competitive as predictive analytics and real-time data inform the logistics decision chain.

Read More →

Commercial Fleet Sales Show Healthy Gains

So far, the fleet sector is outshining government and rental fleet sales this year as economic growth spurs more business investment.

Read More →

CAR 2026 Recap Part 2: Closing the Gap Between Data & Remarketing Value

The second half of CAR 2026 examined how fleets can translate lifecycle strategy, vehicle data, and market shifts into higher real-world results.

Read More →

CAR2026 in Two Words: Velocity, Value (Part 1)

The 2026 Conference of Automotive Remarketing convened with a mandate to involve a new constituency — fleet managers — and an updated mission to demonstrate unrealized value in de-fleeted vehicles.

Read More →