Current Used Vehicle Market Conditions and Outlook

Average auction prices in June were up from year-ago levels for the fourth month in a row, but were lower than in May. According to ADESA Analytical Services’ monthly analysis of Wholesale Used Vehicle Prices by Vehicle Model Class, average auction prices in June were up 1.2 percent from year-ago levels, but down 1.5 percent relative to the previous month.

Average auction prices in June were up from year-ago levels for the fourth month in a row, but were lower than in May. According to ADESA Analytical Services’ monthly analysis of Wholesale Used Vehicle Prices by Vehicle Model Class, average auction prices in June were up 1.2 percent from year-ago levels, but down 1.5 percent relative to the previous month. Car prices generally registered solid gains, with full-size, compact, and sporty cars making the strongest year-over-year price gains. Truck prices – especially for full-size SUVs – showed declines, possibly reflecting high gas prices. Generally more fuel-efficient Mini SUVs were the only truck segment to register double-digit year-over-year price increases, which reinforces this hypothesis.

Retail demand has been one key driver of the overall firming trend in wholesale prices during the last twelve months. ADESA Analytical Services cited May 2003 as an “inflection point” in the market based on our observation at the time that retail used vehicle prices as a percent of new vehicle prices were at historical lows (below 50 percent at franchised dealerships). These relatively low retail prices, along with a recovering economy and other factors, helped stimulate retail used vehicle sales.

Although retail used vehicle sales continue to be brisk, the rate of increase versus year-ago levels has been tapering as we enter the months corresponding to the period after last year’s inflection point. According to data from CNW Marketing/Research, year-over-year retail sales growth has declined from 10.5 percent in April, to 10 percent in May, to 9.3 percent in June. For independent dealers these percentages have gone from 20.1 percent to 16.1 percent to 14.1 percent. It is important to note, however, that on a year-to-date basis through June, independent dealers have sold more vehicles than at any time since CNW has been compiling this data. This is especially encouraging considering that last year through June, independent dealers were suffering through what might have been their worst first-half ever.

The other major driver in the firming price environment is declining supply – primarily from off-lease vehicles. A reflection of this is that the ADESA Auction Inventory Index now stands at 88.3 – 27 percent below its year-ago level, and 17 percent below May month-end. This result was anticipated in ADESA Analytical Services’ 2003 Global Vehicle Remarketing report, where we projected nearly a 230,000-unit drop in off-lease volume between 2003 and 2004.

Auction industry conversion rates (vehicle sold as a percent of vehicles offered) appear to be settling at their historical norm of roughly 40 percent for dealer-to-dealer units and 60 percent for all units processed. A reflection of this is that the ADESA Auction Dealer Optimism Index was down modestly in June after being up for thirteen months in a row. This means that dealers purchased a lower percentage of vehicles offered for sale by other dealers at ADESA auctions than they did last year – another indication that retail demand is tapering to more traditional summer levels after a strong spring.

More Operations

Manheim Index Shows Used-Vehicle Wholesale Prices Up 2.1% in June

The market is seeing stronger appreciation in older used vehicles this year, and the most affordable segments have been among the year’s best performers.

Read More →

Commercial Fleet Sales Contribute To June, YTD Gains

The fleet sector has boosted its vehicle purchases at a reliable pace in the first half of this year compared with 1H 2025.

Read More →

Stop Remarketing Electric Vehicles Like Gas Cars

The advantages and attributes of electric vehicles are upending the traditional remarketing cycle, requiring fleet sellers to rely on new factors and approaches detailed below.

Read More →

AP Fleet Management Expands Remarketing Program for Commercial Work Trucks

AP Fleet Management expanded its commercial vehicle remarketing program with dedicated resale services and an online marketplace for used work trucks.

Read More →

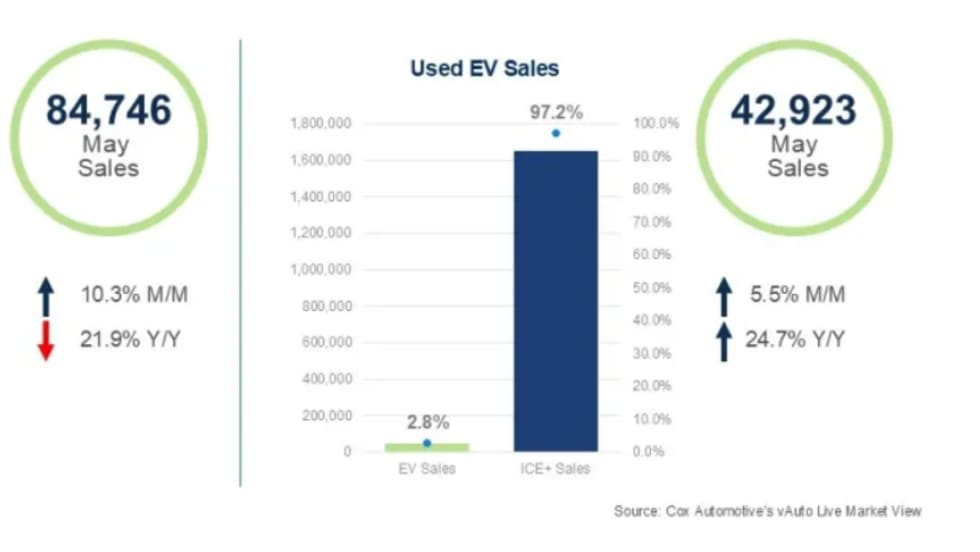

Used EVs Strengthen Overall Electric Vehicle Market

The latest sales data point to several reasons for the divergent trends in new and used EVs that can factor into fleet cycling decisions.

Read More →

The Data-Driven Haul: 5 Ways AI is Leveling the Playing Field in Auto Transport

Large and small transport fleets are becoming more competitive as predictive analytics and real-time data inform the logistics decision chain.

Read More →

2026 CAR Awards Celebrate Industry Excellence

CAR’s annual Fleet Remarketing Awards opened a reimagined 2026 conference designed to bridge the worlds of fleet management and automotive remarketing.

Read More →

CAR 2026 Recap Part 2: Closing the Gap Between Data & Remarketing Value

The second half of CAR 2026 examined how fleets can translate lifecycle strategy, vehicle data, and market shifts into higher real-world results.

Read More →

CAR2026 in Two Words: Velocity, Value (Part 1)

The 2026 Conference of Automotive Remarketing convened with a mandate to involve a new constituency — fleet managers — and an updated mission to demonstrate unrealized value in de-fleeted vehicles.

Read More →

CAR 2026: Get the Wall Street Update on the Key Players in Remarketing

From a Wall Street analyst's take on remarketing's key players to whether fleets need their own version of Carfax, CAR 2026's afternoon roundtables will answer key operational and industry questions.

Read More →