Economic Trends Impacting Resale Values in 2020-2021

The remarketing industry observed a lower number of off-lease units in 2020 than anticipated; fleets extending asset lifecycles; and fewer repossessions than what would occur in a normal year.

Photo courtesy of niekverlaan via Pixabay.

The remarketing industry observed a lower number of off-lease units in 2020 than anticipated; fleets extending asset lifecycles; and fewer repossessions than what would occur in a normal year, as reported at the session on the “Forecast of the Economic Trends that will Impact Resale Values in 2020/2021 Calendar Years” during the virtual 2020 Virtual Conference of Automotive Remarketing (CAR) Experience.

The panel discussion featured Tom Kontos, chief economist at KAR Auction Services; Jonathan Smoke, chief Economist at Cox Automotive; and Mike Antich, conference chair for the CAR Experience, who served as the session’s moderator, and segmented the discussion across various industry segments.

Macroeconomic Overview

The presentation started with both panelists giving an overview on how the general macroeconomy is currently impacting the resale market. Kontos observed that, despite lower levels of employment experienced during the pandemic, consumer spending on homes and cars has sustained.

“With the stimulus package, personal incomes were sustained at a high level, which they would not otherwise have been at. And that high level enabled the kinds of expenditures on cars and homes that we've seen,” Kontos said.

However, he noted, continued strength of the overall macroeconomy may be dependent on the passing of a second stimulus package and future unemployment rates. Smoke echoed Kontos’ thoughts on the subject.

“If you're trying to focus on the most important things to understand where we go from here, unemployment and the timing and size of the next stimulus package are probably the two most important things to track,” said Smoke.

He added that potential continued cases of COVID-19 could also continue to impact how the market will trend in the future, particularly looking ahead to late next year.

“That means that even if we don't have additional problems with further outbreaks by the end of next year, and we just maintain what we've been seeing, it really leads us to what looks like an 80% economy, because 20% of the economy just can't recover,” said Smoke. “Because it's industries like travel and service business that effectively cannot operate as usual until then.”

Off-Lease Units

Before the pandemic hit, Kontos noted that off-lease units in 2020 were expected to be low on a year-over-year basis, but that the pandemic made this reduction even more significant through the year.

“We knew it would be down a bit from the year before, but not a huge amount,” said Kontos. “But then this pandemic hit, and lease maturities were delayed. Those delays reduced the amount of off-lease volumes even more dramatically than we might have seen on a year-over-year basis.”

The increase of off-lease extensions initially created concerns that supply would eventually overwhelm the market.

However the panelists observed a trend of off-lease units being bought by lessees, particularly for those in need of a new vehicle, as well as the take grade for upstream buyers and grounding dealers being high, therefore fewer vehicles made their way to auction. This trend also helped support late-model used car prices.

“As the market recovered, those upstream channels and the take rate at which the consumer was taking the vehicle because it represented such a value has basically meant that the auctions are down,” said Smoke. “We think we'll end the year with the maturities roughly being about what we expected before this year began.”

Because of this, there has not been a build up of “phantom supply” in the off-lease market for the market next year. Smoke noted that the beginning of 2020 was supposed to be the ultimate peak in off-lease maturities as the result of new vehicle sales and leasing being at its peak three years ago

“And so from here, we're going to see less of those vehicles, and actually we think those take rates next year will probably be a bit more consistent. There's going to be plentiful supply, but it's definitely no longer growing,” Smoke said. “And I think we can absolutely say, because of this combined with rental, that 2020 was the peak in the youngest vehicles the industry has had. And we're not likely to return to that, you know, mix of young vehicles for many years.”

Daily Rental Volumes

Declines in travel during the pandemic led to a rapid downsizing in rental units, both for pure rental risk vehicles and and rental vehicles that were being returned to the manufacturers, Smoke observed.

“This was the supply that we saw build up and, and be the bulk of the oversupply that we had for a period of time,” according to Smoke.

The high profile situation of Hertz going into bankruptcy caused a lot of consternation about how much of that was going to impact the market, and whether or not the market could handle it.

Rental risk values saw extreme swings, when compared to the overall market, after rental hit its lowest points earlier in the year.

“But then as the market has recovered, we've seen those rental values recover just as strongly as well,” said Smoke. “And that's because there, there has been plenty of retail demand for the market overall, but also specifically for those younger vehicles. And more importantly, I no longer see rental inventory up on a year-over-year basis, the industry seems to have eaten through most of the inventory. And from what we hear from the rental car companies, we're through most of the big moves to de-fleet. So I actually think that the values are going to be fairly predictable and stable relative to what we've been seeing for the market overall.”

Smoke said he expects the number of rental volumes into the wholesale market, overall, by the end of the year going down by potentially about 300,000 units, and maybe down another 200,000 next year.

“So what seems to be an abundance, maybe earlier in the pandemic of off rental is going to be sort of a scarce commodity in the foreseeable future, well into 2021,” added Kontos.

Fleet Lifecycles Extending

Smoke and Kontos also addressed how some fleets are extending vehicle lifecycles this year.

Kontos noted that the average de-fleeting period for fleet clients that usually occurs in the Fall season may be extended into Spring of 2021. This is driven by a decline in business activity, particularly for fleets of non-essential businesses.

“We know that those vehicles haven't run up the kind of miles where they need to be replaced, which might be based on lifecycle cost analysis,” Kontos said. “Fleet managers and fleet management companies may choose to extend the service life of a car, but then remarket it at a time of the year they think will be strong.”

Smoke echoed Kontos’ sentiments.

“The commercial segment has really been the most stable part of purchase activity. So purchase activity is strong, with the exception of miles traveled being down, and essentially moving the timing a bit for vehicle replacement,” Smoke said.

Repossession Trends

There is an anticipated uptick in repossessions later this year as delinquency moratoriums come to an end, both panelists also observed, though there has been a shift with regards to previous expectation of what the year would look like due to the pandemic.

“Repo has been the biggest downside surprise. Normally, when you have an economic recession, repos are the category that grows,” said Smoke. “But because of the stimulus and because of loan accommodations, we actually are going to end up with fewer repos than we would in a normal year. We think this year is going to end down in repossessions by about 300,000 units, compared to last year when unemployment was 3.5%.”

He also noted that while the 60-day delinquencies have finally ticked up, the delinquency rate is still below pre-pandemic levels and below last year.

“I think it's going to be a function of time, before we get to what would have been the delinquencies and defaults happening in 2020, happening in 2021,” Smoke added. Though Smoke said he doesn't expect default rates to be as high, as consumers may be using stimulus monies to pay down their debts.

“So we don't necessarily have the same number of consumers that would have gotten into trouble,” he added. “But we definitely think it's going to be a source of new vehicles, probably a difference of almost a million more vehicles next year.”

More Operations

Manheim Index Shows Used-Vehicle Wholesale Prices Up 2.1% in June

The market is seeing stronger appreciation in older used vehicles this year, and the most affordable segments have been among the year’s best performers.

Read More →

Commercial Fleet Sales Contribute To June, YTD Gains

The fleet sector has boosted its vehicle purchases at a reliable pace in the first half of this year compared with 1H 2025.

Read More →

Stop Remarketing Electric Vehicles Like Gas Cars

The advantages and attributes of electric vehicles are upending the traditional remarketing cycle, requiring fleet sellers to rely on new factors and approaches detailed below.

Read More →

AP Fleet Management Expands Remarketing Program for Commercial Work Trucks

AP Fleet Management expanded its commercial vehicle remarketing program with dedicated resale services and an online marketplace for used work trucks.

Read More →

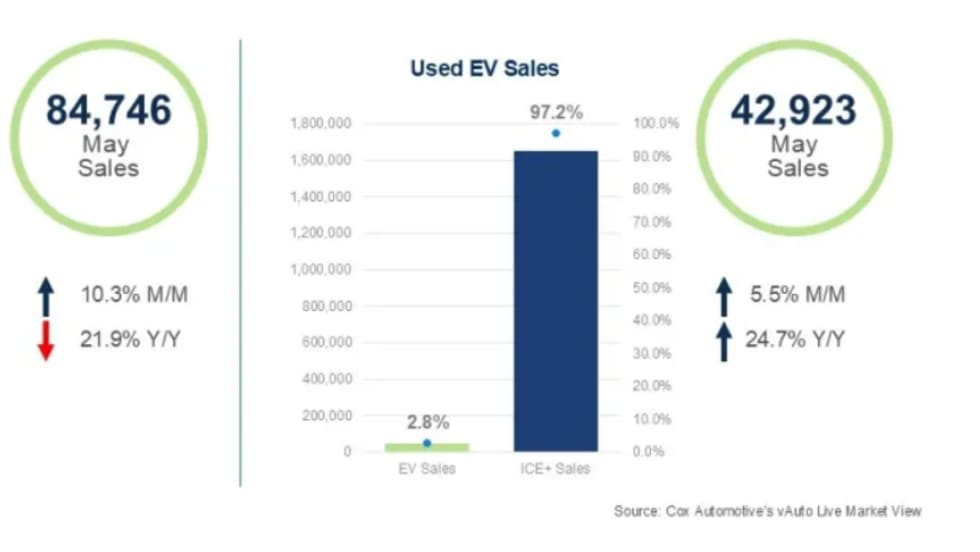

Used EVs Strengthen Overall Electric Vehicle Market

The latest sales data point to several reasons for the divergent trends in new and used EVs that can factor into fleet cycling decisions.

Read More →

The Data-Driven Haul: 5 Ways AI is Leveling the Playing Field in Auto Transport

Large and small transport fleets are becoming more competitive as predictive analytics and real-time data inform the logistics decision chain.

Read More →

2026 CAR Awards Celebrate Industry Excellence

CAR’s annual Fleet Remarketing Awards opened a reimagined 2026 conference designed to bridge the worlds of fleet management and automotive remarketing.

Read More →

CAR 2026 Recap Part 2: Closing the Gap Between Data & Remarketing Value

The second half of CAR 2026 examined how fleets can translate lifecycle strategy, vehicle data, and market shifts into higher real-world results.

Read More →

CAR2026 in Two Words: Velocity, Value (Part 1)

The 2026 Conference of Automotive Remarketing convened with a mandate to involve a new constituency — fleet managers — and an updated mission to demonstrate unrealized value in de-fleeted vehicles.

Read More →

CAR 2026: Get the Wall Street Update on the Key Players in Remarketing

From a Wall Street analyst's take on remarketing's key players to whether fleets need their own version of Carfax, CAR 2026's afternoon roundtables will answer key operational and industry questions.

Read More →