More News: Used Vehicle Supply Rises, Average Listing Price Dips

Wholesale Used-Vehicle Prices Decline in February

Combined sales into large rental, commercial, and government buyers were down 30% year over year in February. Sales into rental were down 52% YOY.

March 7, 2022

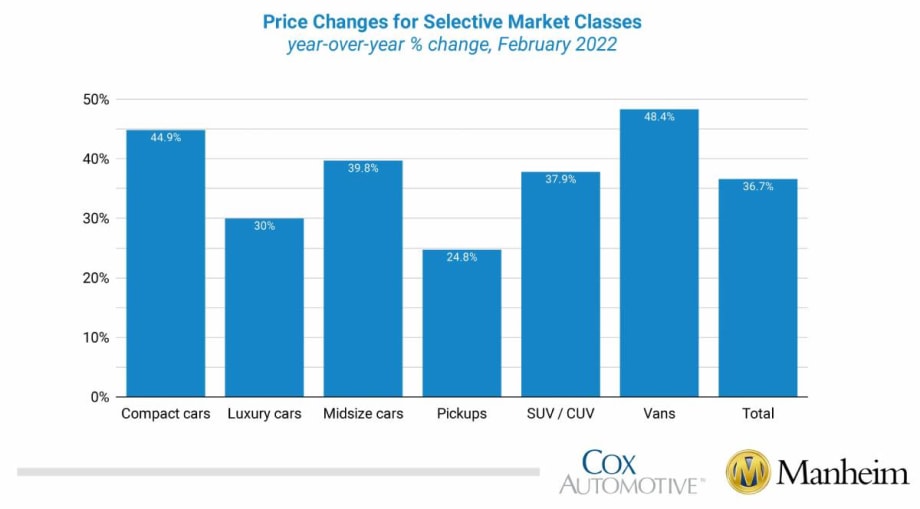

All major market segments saw seasonally adjusted prices that were higher year over year in February. Vans had the largest year-over-year performance, followed by compact cars, while pickups, luxury cars, and sports cars lagged the overall market. On a month-over-month basis, all major segments saw price declines.

Source: Cox/Manheim

4 min to read

Wholesale used-vehicle prices (on a mix-, mileage-, and seasonally adjusted basis) declined 2.1% in February from January, Cox Automotive reported March 7. The Manheim Used Vehicle Value Index declined to 231.3, which was a 36.7% increase from a year ago. The non-adjusted price change in February was a decline of 2.2% compared to January, leaving the unadjusted average price up 32.4% year over year.

Manheim Market Report (MMR) values saw weekly price decreases in February that decelerated each week. Over the last four weeks, the Three-Year-Old Index declined a net 2.6%. Over the month of February, daily MMR Retention, which is the average difference in price relative to current MMR, averaged 98.4%, which meant that market prices were behind MMR values. The average daily sales conversion rate declined in the month to 49.1%, which was below normal for the time of year. For example, the sales conversion rate averaged 53% in February 2019. The lower conversion rate indicates that the month saw buyers with more bargaining power for this time of year, and as a result, most vehicles showed price depreciation. However, price patterns in the month varied by vehicle age and segment. Older vehicles were more likely to see price stability, while younger vehicles tended to see larger declines.

All major market segments saw seasonally adjusted prices that were higher year over year in February. Vans had the largest year-over-year performance, followed by compact cars, while pickups, luxury cars, and sports cars lagged the overall market. On a month-over-month basis, all major segments saw price declines.

Retail used sales down in February with slow start to tax refund season. Leveraging a same store set of dealerships selected to represent the country from Dealertrack, Cox estimates that used retail sales increased 3% in February from January but failed to show the typical seasonal increase driven by tax refund season. The Dealertrack estimates indicate that used retail sales were down 7% year over year. Consistent with this performance, the issuance of tax refunds is less than half of what we typically would see this time of year. Based on IRS statistics through Feb. 18, we estimate that 17% of this year’s likely number of tax refunds have been issued, when for the same week in 2019, 38% had been distributed. The market will eventually see strong used-vehicle demand from tax refunds being issued, as the average refund so far this year is up 13% year over year.

Using estimates of used retail days’ supply based on vAuto data, January ended at 58 days, which is higher than how January 2021 ended at 44 days. Retail supply had declined to 55 days as of mid-February, which was still higher than mid-February 2021 at 48 days. Leveraging Manheim sales and inventory data, Cox estimates that wholesale supply ended February at 28 days, which is higher than how February 2021 ended at 25 days but lower than how January ended at 31 days.

February total new-light-vehicle sales were down 12% year over year, with the same number of selling days compared to February 2021. By volume, February new-vehicle sales were up 6% over January. The February SAAR came in at 14.1 million, an 11% decline from last year’s 15.9 million, and down 6% from January’s 15 million pace.

Combined sales into large rental, commercial, and government buyers were down 30% year over year in February. Sales into rental were down 52% year over year, while sales into commercial and government fleets had modest year-over-year gains of 1% and 8%, respectively. Including an estimate for fleet deliveries into the dealer and manufacturer channel, Cox estimates that the remaining retail sales were down 8% year over year in February, leading to an estimated retail SAAR of 12.2 million, which was down from 13.2 million last February and also last month’s 13.2 million rate.

Rental risk mileage stable: The average price for rental risk units sold at auction in February was up 32% year over year. Rental risk prices were down 4% compared to January. Average mileage for rental risk units in February (at 59,300 miles) was up 13% compared to a year ago but unchanged from January.

Consumer sentiment fell again in February: Consumer Confidence according to the Conference Board declined 0.5% in February. The underlying measures of present situation and future expectations moved in opposite directions as present situation improved but future expectations declined. Plans to purchase a vehicle in the next six months declined and are now down year over year. The consumer sentiment index from the University of Michigan declined 8.1% in February as both current conditions and expectations declined. The Michigan reading was up from mid-month but recorded the lowest full-month reading since August 2011. The Morning Consult daily index also declined in February, as it declined 1.7% in the final week of the month and ended down 1.3% for the month and down 9.1% year over year.

More Auctions

Used Vehicle Prices Climb Higher As Sales Pace Slows

The higher prices at used retail reflect strong wholesale values earlier in the spring, particularly for older, more affordable vehicles.

Read More →

Wholesale Used Vehicle Market Sustains Moderate Rise In Values, Prices

Trends continue to normalize after a strong start to the year, as consumers contend with higher gas prices in the coming summer months.

Read More →

Wholesale Used Vehicle Prices Slightly Up In April

The Iranian conflict and rising gas prices inject much uncertainty into the future wholesale used vehicle markets, as higher gas prices soak up spendable income from vehicle buyers.

Read More →

The Predictive Pivot: How AI and Data Are Redefining Auto Logistics in 2026

AI is no longer a luxury but the baseline for profitability in 2026. Auto haulers that adopt these tools now will quickly outpace those using manual workflows and taking a wait-and-see approach.

Read More →

CAR2026 in Two Words: Velocity, Value (Part 1)

The 2026 Conference of Automotive Remarketing convened with a mandate to involve a new constituency — fleet managers — and an updated mission to demonstrate unrealized value in de-fleeted vehicles.

Read More →

CAR 2026 Session to Uncover the Missing Data That's Costing Fleets at Disposal

Work trucks lose value at remarketing, not because they aren't worth more, but because the data to prove it rarely makes it to the auction.

Read More →

TSD Mobility, UVeye Partner On Automated Vehicle Inspections

The enhanced technology allows rental car operations, dealerships, and auctions to compare a vehicle’s condition at pickup and drop-off within the same rental or loaner record.

Read More →

Auction Sales Kick Off 2026 In High Step

Winter snowstorms and frosty freeze-overs could not slow down the hot vehicle auction action nationwide in January.

Read More →

Plug Raises Capital To Grow Its Used EV Marketplace

The $20 million in Series A funding from Lightspeed will enable Plug to boost supply, develop more technology, and widen wholesale and retail sales channels.

Read More →

Nomination Deadline Approaches for 2026 Fleet Remarketing Awards at CAR

The 2026 Fleet Remarketing Award Nominations will close on March 1. The awards recognize industry leadership, highlighted by a new award focused on fleet vehicle value creation.

Read More →