Results of Consumer Bankers Association 2007 Automobile Finance Study

ATLANTA– BenchMark Consulting International, a management consulting firm to the financial services industry, announced the results of the Consumer Bankers Association 2007 Automobile Finance Study. Conducted by BenchMark Consulting International for the Consumer Bankers Association (CBA), the study examines data on a multi-year basis for indirect lending, leasing and floorplan finance.

ATLANTA– BenchMark Consulting International, a management consulting firm to the financial services industry, announced the results of the Consumer Bankers Association 2007 Automobile Finance Study. Conducted by BenchMark Consulting International for the Consumer Bankers Association (CBA), the study examines data on a multi-year basis for indirect lending, leasing and floorplan finance.

The results point to contraction in the market. Overall, indirect lending portfolio dollars were down 7 percent, year-over-year, with large-class respondents reporting a 15-percent decrease in dollars since last year's study. All areas of origination – approval-to-application, booking-to-approval and booking-to-application – have been trending downward since last year's study, with 6-percent, 22-percent and 27-percent declines, respectively, in weighted averages.

The study shows that new-car-loan maturities longer than five years rose to 58 percent in 2006 (up 6 percent from last year) and account for the highest percentage of all term categories for new loans. Average new-loan maturities continue to trend upward for loans of more than 60 months, with the average maximum maturity for new car loans standing at 79 months at year-end.

Elaborating on the findings, BenchMark President Walter Cunningham said, "To a great extent competition on pricing and terms has driven this trend. However, negative-equity situations from prior extended terms, quicker movement to smaller cars and falling 'big' vehicle prices have also contributed to this pattern.”

The increase in longer-term loans poses some specific issues for financial institutions. "Our findings indicate that consumer behaviors such as slower repayment, longer negative equity and 'walking away from the loan' inevitably increase in this environment,” said Cunningham. "On the industry side, business is impacted by slower future vehicle sales, reduced future down payments, greater severity of loss on repossessions and lower overall credit standards.”

The results of the survey also showed a spike in indirect loans in the under-600 FICO score segment, with both new and used loans doubling in percentage by year-end 2006. "With the continued deterioration of subprime credit segments, a careful eye should be kept on this area of auto financing,” cautioned Cunningham.

Indeed, the study found a 16-percent increase in loan delinquency dollars for new vehicles and 18 percent for used vehicles. According to participants who provided such data, gross charge-off rates continued their three-year increase, with a 7-percent increase since the last study. Additionally, the study found 17 percent more applications were dealer-entered over year-end 2005. There was also a 17-percent increase in the number of respondents who allowed dealers to approve loans without initial intervention – which Cunningham noted may be a reflection of increased efficiencies and improved dealer-lender communications.

For more information about the 2007 CBA Automobile study results, contact Beth Riedemann at b-riedemann@benchmarkinternational.com.

More Operations

Manheim Index Shows Used-Vehicle Wholesale Prices Up 2.1% in June

The market is seeing stronger appreciation in older used vehicles this year, and the most affordable segments have been among the year’s best performers.

Read More →

Commercial Fleet Sales Contribute To June, YTD Gains

The fleet sector has boosted its vehicle purchases at a reliable pace in the first half of this year compared with 1H 2025.

Read More →

Stop Remarketing Electric Vehicles Like Gas Cars

The advantages and attributes of electric vehicles are upending the traditional remarketing cycle, requiring fleet sellers to rely on new factors and approaches detailed below.

Read More →

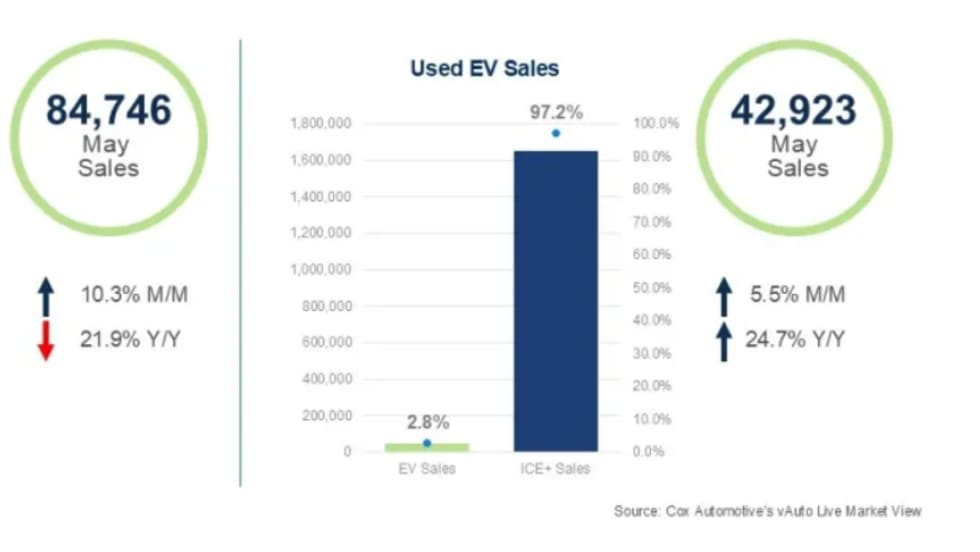

Used EVs Strengthen Overall Electric Vehicle Market

The latest sales data point to several reasons for the divergent trends in new and used EVs that can factor into fleet cycling decisions.

Read More →

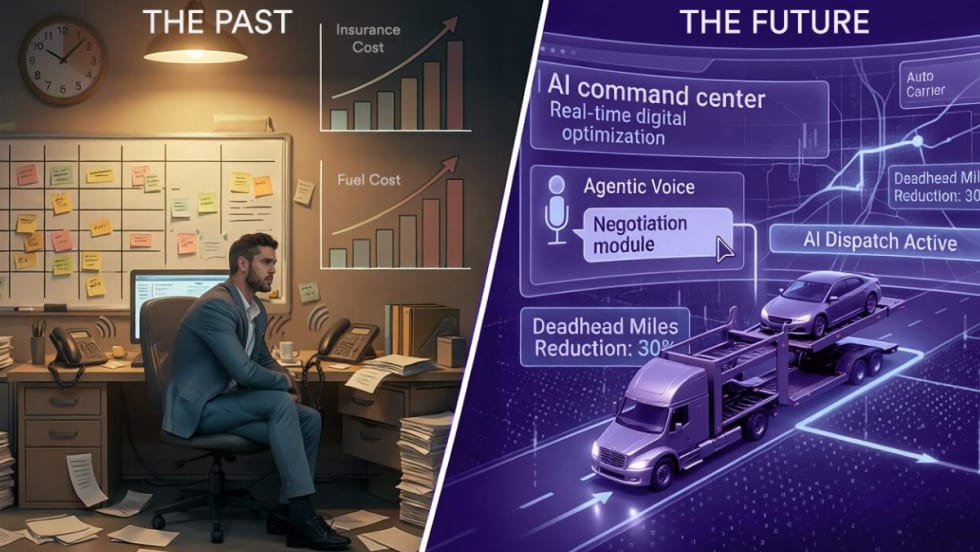

The Data-Driven Haul: 5 Ways AI is Leveling the Playing Field in Auto Transport

Large and small transport fleets are becoming more competitive as predictive analytics and real-time data inform the logistics decision chain.

Read More →

2026 CAR Awards Celebrate Industry Excellence

CAR’s annual Fleet Remarketing Awards opened a reimagined 2026 conference designed to bridge the worlds of fleet management and automotive remarketing.

Read More →

The Predictive Pivot: How AI and Data Are Redefining Auto Logistics in 2026

AI is no longer a luxury but the baseline for profitability in 2026. Auto haulers that adopt these tools now will quickly outpace those using manual workflows and taking a wait-and-see approach.

Read More →

CAR 2026 Recap Part 2: Closing the Gap Between Data & Remarketing Value

The second half of CAR 2026 examined how fleets can translate lifecycle strategy, vehicle data, and market shifts into higher real-world results.

Read More →

CAR2026 in Two Words: Velocity, Value (Part 1)

The 2026 Conference of Automotive Remarketing convened with a mandate to involve a new constituency — fleet managers — and an updated mission to demonstrate unrealized value in de-fleeted vehicles.

Read More →

CAR 2026: Get the Wall Street Update on the Key Players in Remarketing

From a Wall Street analyst's take on remarketing's key players to whether fleets need their own version of Carfax, CAR 2026's afternoon roundtables will answer key operational and industry questions.

Read More →