J.D. Power: Affordability Behind Overall Strength of Used Market

The used-vehicle market has performed exceptionally well so far in 2018, with J.D. Power Valuation Services’ Adjusted Used Vehicle Price Index reaching 119.3 through July. That’s 4.7 percentage points above year-ago levels and 4.8 points above January’s reading.

Compact car prices are up 9.1% from January’s level, followed by midsize and large car gains of 7.3% and 7%, respectively.

By Eric Gandarilla.

The used-vehicle market has performed exceptionally well so far in 2018, with J.D. Power Valuation Services’ Adjusted Used Vehicle Price Index reaching 119.3 through July. That’s 4.7 percentage points above year-ago levels and 4.8 points above January’s reading.

The firm noted that used-vehicle prices began showing strength in the middle half of 2017, and the trend has continued deep into this year’s summer selling season. Most of the segment’s strength has been driven by mainstream car growth, the firm noted, with passenger cars of all sizes experiencing sizable improvements this year.

Compact car prices are up 9.1% from January’s level, followed by midsize and large car gains of 7.3% and 7%, respectively. Mainstream utility prices have also shown significant movement, although not nearly at the same level as their car counterparts. For example, year-to-date compact utility prices have increased by 2.8%, while midsize utility price growth has reached 3.1%.

And while things are primarily positive on the mainstream side of the market, the large SUV segment has registered a 2.2% decline, which can be largely explained by a 28% increase in zero to five-year-old wholesale volume. Luxury segments are also not faring so well.

“Luxury segments are not enjoying the same trend as their mainstream counterparts, due in part to higher incentive spend on the new side of the market,” the firm noted in its report. “Nearly all luxury segments have experienced declines in 2018.”

Like the segment’s mainstream counterpart, luxury large utility prices have deteriorated the most and are down 5.6% from January’s level. Luxury compact utility prices are down 2% so far this year. Other luxury segment losses haven’t been as severe, and prices for the collective are down by roughly 1% year to date, according to the firm.

“There are few drivers behind the overall strength of the used market,” the firm said. “Two primary reasons are an increased dealer focus on used-vehicle operations and vehicle affordability.

“Used vehicles continue to gain popularity with consumers and dealers alike,” the firm added. “Consumers can save money buying a well-maintained, late-model used vehicle, while dealers can capitalize on used-vehicle sales where profit margins are higher than new-vehicle sales.”

With a 4% increase in overall wholesale auction volume for units up to five years old through July, consumers and dealers alike have a slew of late-model cars, SUVs and trucks to choose from — and for up to 50% or more off their original MSRPs.

The firm noted that many of the country’s top public dealership groups are capitalizing on this dynamic, and the benefits were apparent in their latest earnings reports, the firm noted.

In their second-quarter earnings reports, Penske Automotive Group, Group 1 Automotive, and Sonic Automotive Inc. each increased used-vehicle sales by sizable amounts, up 10%, 13%, and 17%, respectively. And while Lithia Motors Inc. and Asbury Automotive Group Inc. posted smaller gains of 4.4% and 7%, respectively, they were impressive nonetheless.

“Each dealer group credited increased used-vehicle operations for the increase in profits, and they continue to state plans for even bigger investments in used operations in the future,” the first stated in its report.

“While the used market is doing well, the year’s improvement highlights the need for stakeholders to maintain diligence in their understanding of market dynamics and trends expected in the future,” the firm added. “To that end, J.D. Power Valuation Services expects used-vehicle prices for units up to eight years in age to increase 1% in 2018 relative to 2017.”

The firm said negatives associated with weaker credit conditions, modestly higher incentives and yet another increase in used-vehicle are expected to be offset by positives associated with strong employment, home prices, driving demand, and continued increases in vehicle quality. Gas prices are expected to have a relatively neutral impact.

“Both mainstream and luxury segment prices are expected to be softer for utilities as more units return to the used market,” the firm noted. “Mainstream passenger car prices should continue to firm up as supply falls, while luxury prices will soften due to the increased competitive pressure associated with luxury utilities as well as mainstream cars whose prices are lower, yet whose design and optional equipment continues to push into luxury territory.

“Overall, 2018 should see used-vehicle prices rebound back to levels recorded two years ago, placing them 5% below the record high observed in 2014.”

This story originally ran on F&I and Showroom, another Bobit Business Media publication.

More Used Vehicle Values

What Happens When Residual Values Meet Real-World Markets

A truck's trade value isn't determined on turn-in day. Learn how market cycles, maintenance, and timing shape the gap between residuals and reality.

Read More →

Manheim Index Shows Used-Vehicle Wholesale Prices Up 2.1% in June

The market is seeing stronger appreciation in older used vehicles this year, and the most affordable segments have been among the year’s best performers.

Read More →

Stop Remarketing Electric Vehicles Like Gas Cars

The advantages and attributes of electric vehicles are upending the traditional remarketing cycle, requiring fleet sellers to rely on new factors and approaches detailed below.

Read More →

Used Vehicle Prices Climb Higher As Sales Pace Slows

The higher prices at used retail reflect strong wholesale values earlier in the spring, particularly for older, more affordable vehicles.

Read More →

Wholesale Used Vehicle Market Sustains Moderate Rise In Values, Prices

Trends continue to normalize after a strong start to the year, as consumers contend with higher gas prices in the coming summer months.

Read More →

Used EV Sales Grow In April

While EV sales declined, used EV sales grew, as tighter inventory and rising prices reflected a more normalized pace for the EV market.

Read More →

Wholesale Used Vehicle Prices Slightly Up In April

The Iranian conflict and rising gas prices inject much uncertainty into the future wholesale used vehicle markets, as higher gas prices soak up spendable income from vehicle buyers.

Read More →

CAR 2026 Recap Part 2: Closing the Gap Between Data & Remarketing Value

The second half of CAR 2026 examined how fleets can translate lifecycle strategy, vehicle data, and market shifts into higher real-world results.

Read More →

CAR2026 in Two Words: Velocity, Value (Part 1)

The 2026 Conference of Automotive Remarketing convened with a mandate to involve a new constituency — fleet managers — and an updated mission to demonstrate unrealized value in de-fleeted vehicles.

Read More →

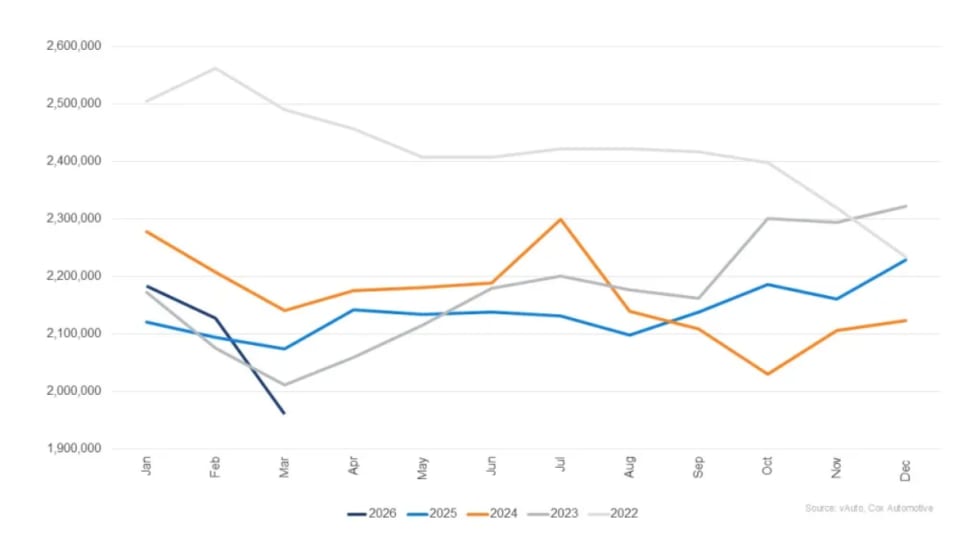

March Used Vehicle Inventory Falls To Lowest Since 2019

Franchised and independent dealers had a total of 1.95 million used vehicles in stock in March, the lowest on record in the current data set.

Read More →