Wholesale Used-Vehicle Prices Decline This Month

Mid-Month Update: The Manheim Used Vehicle Value Index was down 7% compared to the full month of May 2022.

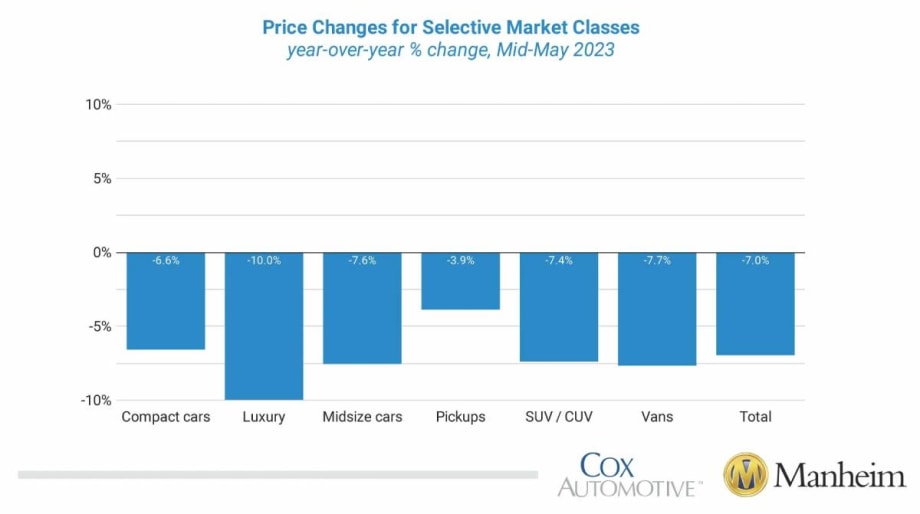

All eight major market segments saw seasonally adjusted prices that were again lower year over year in the first half of May.

Graphic: Cox Automotive

Wholesale used-vehicle prices (on a mix-, mileage-, and seasonally adjusted basis) decreased 2.1% from April in the first 15 days of May, according to the midmonth Manheim Used Vehicle Value Index released May 17.

The index dropped to 225.9, which was down 7% from the full month of May 2022. The seasonal adjustment contributed to the decline. The non-adjusted price change in the first half of May declined 0.9% compared to April, while the unadjusted price was down 7.5% year over year.

Over the last two weeks, Manheim Market Report (MMR) prices were nearly unchanged compared to the end of April. Prices in the first two weeks of May have been generally flat over the last four years, with average changes between ‑0.1% and 0.1% since 2019.

Over the first 15 days of May, MMR Retention, the average difference in price relative to current MMR, averaged 99%, indicating that valuation models remain slightly ahead of market prices. The average daily sales conversion rate of 59.5% in the first half of May declined relative to April’s daily average of 60.3% and was below the May 2019 daily average of 59.9%.

Prices Decline in All Eight Vehicle Segments

All eight major market segments saw seasonally adjusted prices that were again lower year over year in the first half of May. Only pickups and compact cars, at 3.9% and 6.6%, respectively, lost less compared to the overall industry in seasonally adjusted year-over-year changes.

The remaining segments lost between 7.4% and 14.3%, with sports cars losing the most. Seven of the eight major segments saw price decreases compared to April, with losses ranging from 1.7% to 7.0%, while vans were flat.

Retail Used-Vehicle Supply Lower in Mid-May

Using estimates based on vAuto data as of May 8, used retail days’ supply was 43 days, which was down one day from the end of April. Days’ supply was down eight days year over year and down three days compared with the same week in 2019.

Leveraging Manheim sales and inventory data, Manheim estimates that wholesale supply ended April at 25 days, up two days from the end of March and down one day year over year. As of May 15, wholesale supply was at 24 days, down one day from the end of April, down two days year over year, and flat compared to 2019.

Used retail supply measured in days’ supply and compared to 2019 suggests supply is slightly below normal for this time of year, indicating some mismatch between demand and supply despite persistent but improving low inventory levels.

Rental Risk Prices Increase Again in First Half of May

The average price for rental risk units sold at auction in the first 15 days of May was up 3.7% year over year. Rental risk prices were up 1.7% compared to the full month of April. Average mileage for rental risk units in the first half of May (at 58,500 miles) was down 7.9% compared to a year ago and down 1.9% month over month.

Tax Refunds in 2023 Down Compared to Last Year

While the 2023 tax refund season started faster than last year in terms of distribution of refunds, 2023 is behind 2022 on all key metrics. With statistics through the week ending May 5, $263 billion in refunds have been issued. The number of refunds issued is down 1% from last year, 8% less has been disbursed than last year, and the average refund at $2,803 is down 7% year over year.

More Used Vehicle Values

Used Vehicle Prices Climb Higher As Sales Pace Slows

The higher prices at used retail reflect strong wholesale values earlier in the spring, particularly for older, more affordable vehicles.

Read More →

Wholesale Used Vehicle Market Sustains Moderate Rise In Values, Prices

Trends continue to normalize after a strong start to the year, as consumers contend with higher gas prices in the coming summer months.

Read More →

Used EV Sales Grow In April

While EV sales declined, used EV sales grew, as tighter inventory and rising prices reflected a more normalized pace for the EV market.

Read More →

Wholesale Used Vehicle Prices Slightly Up In April

The Iranian conflict and rising gas prices inject much uncertainty into the future wholesale used vehicle markets, as higher gas prices soak up spendable income from vehicle buyers.

Read More →

CAR 2026 Recap Part 2: Closing the Gap Between Data & Remarketing Value

The second half of CAR 2026 examined how fleets can translate lifecycle strategy, vehicle data, and market shifts into higher real-world results.

Read More →

CAR2026 in Two Words: Velocity, Value (Part 1)

The 2026 Conference of Automotive Remarketing convened with a mandate to involve a new constituency — fleet managers — and an updated mission to demonstrate unrealized value in de-fleeted vehicles.

Read More →

March Used Vehicle Inventory Falls To Lowest Since 2019

Franchised and independent dealers had a total of 1.95 million used vehicles in stock in March, the lowest on record in the current data set.

Read More →

Spring Bounce Pushes Q1 Used Vehicle Values Higher

Demand signals remain strong at auctions, with sales conversions, a clear sign of demand, reaching 68.2% in the most recent measure.

Read More →

CAR 2026: Get the Wall Street Update on the Key Players in Remarketing

From a Wall Street analyst's take on remarketing's key players to whether fleets need their own version of Carfax, CAR 2026's afternoon roundtables will answer key operational and industry questions.

Read More →

CAR 2026 Session to Uncover the Missing Data That's Costing Fleets at Disposal

Work trucks lose value at remarketing, not because they aren't worth more, but because the data to prove it rarely makes it to the auction.

Read More →