More News: Fleet Sales Surge as Supply Spikes

Wholesale Used-Vehicle Prices Lurch Upward in February

The month also ended at near 41 days’ vehicle supply, down from 48 days at the end of January and 13 days lower than February 2022 at 54 days' supply.

March 7, 2023

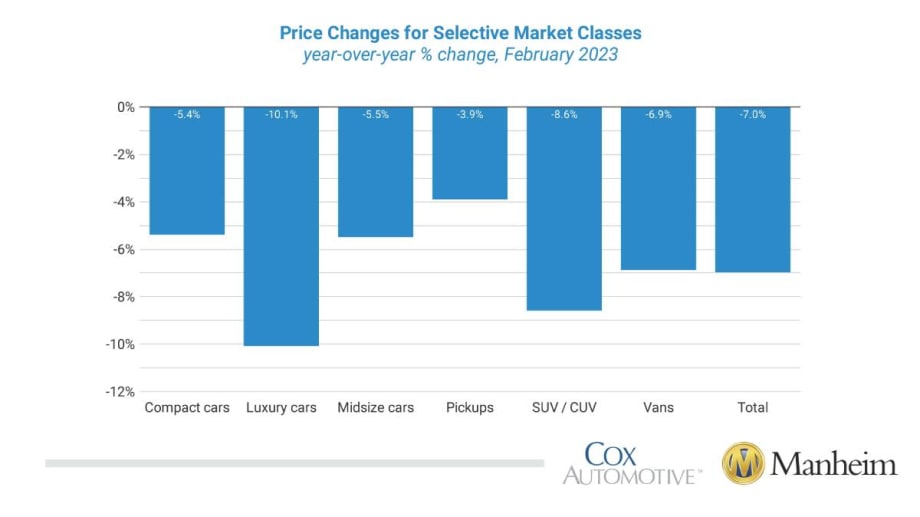

All eight major market segments continued to see seasonally adjusted prices that were lower year over year in February. All eight major segments saw significant price increases compared to January, with gains of between 3.3% and 5.9%.

Graphic: Cox Automotive

4 min to read

Wholesale used-vehicle prices (on a mix, mileage, and seasonally adjusted basis) increased 4.3% in February from January, which was the largest increase for the full month of February since 2009’s 4.4% rise.

The Manheim Used Vehicle Value Index (MUVVI) rose to 234.5, down 7% from a year ago, according to figures released March 7. February’s increase was driven partially by the seasonal adjustment. The non-adjusted price change in February was an increase of 3.7% compared to January, moving the unadjusted average price down 5.6% year over year.

In February, Manheim Market Report (MMR) values saw increases that were not typical, culminating in a 2.4% increase in the Three-Year-Old Index over the last four weeks. During February, daily MMR Retention, which is the average difference in price relative to the current MMR, averaged 100.1%, meaning market prices were very close to MMR values. The average daily sales conversion rate increased to 64.3% and was above normal for the time of year. For example, the daily sales conversion rate averaged 55.3% in January 2019. The higher conversion rate indicated that the month saw sellers with more pricing power than what is typically seen for this time of year.

All eight major market segments continued to see seasonally adjusted prices that were lower year over year in February. Pickups had the smallest decline at 3.9%, with compact cars, midsize cars, and vans losing less than the overall industry year over year. Luxury cars, SUVs, and sports cars lost 10.1%, 8.6%, and 7.4% respectively, compared to last February. All eight major segments saw big price increases compared to January, with gains of between 3.3% and 5.9%.

Used Retail Vehicle Sales Declined in February

Leveraging a same-store set of dealerships selected to represent the country from Dealertrack, used retail sales declined 5% in February from January and were down 9% year over year.

Using estimates of used retail days’ supply based on vAuto data, an initial analysis indicates February ended near 41 days’ supply, down from 48 days at the end of January and 13 days lower than how February 2022 ended at 54 days. Leveraging Manheim sales and inventory data, wholesale supply is estimated to have finished February at 24 days, down two days from the end of January and down five days from how February 2022 ended at 29 days.

February’s total new-light-vehicle sales were up 8.7% year over year, with the same number of selling days as February 2022. By volume, February new-vehicle sales were up 9.1% from January. The February sales pace, or seasonally adjusted annual rate (SAAR), came in at 14.9 million, an 8.5% increase from last year’s 13.7 million but down 6.2% from January’s revised 15.9 million pace.

Combined sales into large rental, commercial, and government fleets increased 48% year over year in February. Sales into rental fleets were up 77% year over year, sales into commercial fleets were up 23%, and sales into government fleets were up 42%. Including an estimate for fleet deliveries into dealer and manufacturer channels, the remaining retail sales were estimated to be up 4.3%, leading to an estimated retail SAAR of 12.3 million, up 0.5 million from last year’s pace but down 0.9 million from last month’s pace. The fleet market share of 17.7% was a 3.5% gain compared to last year’s share of 14.2% and was a 1.2% increase from last month’s estimated 16.5% market share.

Rental Risk Prices and Mileage Rise Substantially in February

The average price for rental risk units sold at auction in February was up 0.5% year over year. Rental risk prices were up 5% compared to January. Average mileage for rental risk units in February (at 60,700 miles) was up 2.4% compared to a year ago and up 8.8% from January.

Measures of Consumer Confidence Mixed in February

The Conference Board Consumer Confidence Index declined 2.9% in February, as views of present situation improved but future expectations fell by 8.3%. Plans to purchase a vehicle in the next six months fell to the lowest level since November 2021. The confidence index did not decline as much during the pandemic as the sentiment index from the University of Michigan, but that series has improved every month this year. The Michigan index increased 3.2% in February and was up 6.7% year over year. Consumers’ views of buying conditions for vehicles declined modestly in February but remained much better than a year ago. The daily index of consumer sentiment from Morning Consult measured improving sentiment in February following a slight decline in January. That index increased 3.2% in February as the price of gasoline declined. The national average price for unleaded gas fell 4.1% in February to $3.36 per gallon on Feb. 28, down 7% year over year, according to AAA.

More Used Vehicle Values

Used Vehicle Prices Climb Higher As Sales Pace Slows

The higher prices at used retail reflect strong wholesale values earlier in the spring, particularly for older, more affordable vehicles.

Read More →

Wholesale Used Vehicle Market Sustains Moderate Rise In Values, Prices

Trends continue to normalize after a strong start to the year, as consumers contend with higher gas prices in the coming summer months.

Read More →

Used EV Sales Grow In April

While EV sales declined, used EV sales grew, as tighter inventory and rising prices reflected a more normalized pace for the EV market.

Read More →

Wholesale Used Vehicle Prices Slightly Up In April

The Iranian conflict and rising gas prices inject much uncertainty into the future wholesale used vehicle markets, as higher gas prices soak up spendable income from vehicle buyers.

Read More →

CAR 2026 Recap Part 2: Closing the Gap Between Data & Remarketing Value

The second half of CAR 2026 examined how fleets can translate lifecycle strategy, vehicle data, and market shifts into higher real-world results.

Read More →

CAR2026 in Two Words: Velocity, Value (Part 1)

The 2026 Conference of Automotive Remarketing convened with a mandate to involve a new constituency — fleet managers — and an updated mission to demonstrate unrealized value in de-fleeted vehicles.

Read More →

March Used Vehicle Inventory Falls To Lowest Since 2019

Franchised and independent dealers had a total of 1.95 million used vehicles in stock in March, the lowest on record in the current data set.

Read More →

Spring Bounce Pushes Q1 Used Vehicle Values Higher

Demand signals remain strong at auctions, with sales conversions, a clear sign of demand, reaching 68.2% in the most recent measure.

Read More →

CAR 2026: Get the Wall Street Update on the Key Players in Remarketing

From a Wall Street analyst's take on remarketing's key players to whether fleets need their own version of Carfax, CAR 2026's afternoon roundtables will answer key operational and industry questions.

Read More →

CAR 2026 Session to Uncover the Missing Data That's Costing Fleets at Disposal

Work trucks lose value at remarketing, not because they aren't worth more, but because the data to prove it rarely makes it to the auction.

Read More →