Are You Over-Depreciating Your Vehicles?

When a company acquires an asset, or the use of an asset, whose value declines over time, that value must be appropriately reduced on the company's books. Vehicles are, without question, assets whose value decreases with use, and fleet managers must make the determination as to how quickly to reduce the original cost.

When a company acquires an asset, or the use of an asset, whose value declines over time, that value must be appropriately reduced on the company's books. Vehicles are, without question, assets whose value decreases with use, and fleet managers must make the determination as to how quickly to reduce the original cost.

What is Depreciation?

There are two categories of depreciation: actual depreciation, which is the difference between the original value and the proceeds from resale, and "book" depreciation, which is the amount by which the original value is reduced, in regular increments, on the company's balance sheet or as monthly expense. Obviously, actual depreciation cannot be determined until the vehicle has been removed from service and sold. Tracking actual depreciation is a critical process, as past depreciation history will help determine future book depreciation. Book depreciation is an accounting function, whereby the company recognizes the expense associated with declining asset value on a monthly basis.

A basic tenet of accounting requires that expense be recognized in the period in which it occurs. It is therefore incumbent upon the fleet manager to establish a depreciation rate that, as accurately as possible, reflects the actual rate at which the vehicle will ultimately lose value. Unfortunately, it is often the case that, due to common industry practice, fleet vehicles are depreciated at rates that do not accomplish this.

The 50-Month (2%) Trap

As with any other industry, there are a number of practices in the fleet industry which, over the years, have become almost defaults in process. One of these common practices is that of depreciating vehicles over a 50-month period, or 2 percent per month. This came about back when the fledgling fleet leasing industry was leasing primarily sales and management automobiles, which were replaced in roughly two years, and generally retained about 60 percent of their original value. Lessors, in open-end leases, recommended a 50-month amortization rate, which would result in that 60-percent residual value. This, over the years, has become the most commonly used depreciation rate for autos, and has crept over into light trucks and vans as well.

But fleet vehicles have become a much more eclectic mix in the last decade, with minivans, more light trucks, sport/utility vehicles, and other types of vehicles taking a larger portion of the fleet mix. In addition, vehicles now are run well beyond three years, and are being replaced at much higher mileages, with the result being that actual depreciation rates varying greatly from the aforementioned 50-month standard have become commonplace. A vehicle whose value retention is 60 percent after two years in service might retain 45 or 50 percent after three years; if depreciated at a 50-month rate, the "book" value would decline to 36 percent, clearly not a very good accounting match.

For example, assume a vehicle whose original cost is $15,000 is replaced at 24 months, at which time its market value is $8,000. A 50- month depreciation rate would result in a minor adjustment at resale time:

$15,000 / 50 = $300

$300 X 24 = $7,200

$15,000 - $7,200 = $7,800 undepreciated book value

$8,000 minus $7,800 = $200

The rate of depreciation in the marketplace will decline as the vehicle ages. Our sample fleet vehicle will have experienced the bulk of its depreciation in the first year to 18 months; after that, the rate of depreciation will decline. Thus, if the company decides to extend the replacement cycle from two to three years, the additional year will be kinder to the market value than were the first two, and, unless the depreciation rate is adjusted accordingly, over-depreciation will result. In our sample case, the third year depreciation rate in the market will not likely be as high as it was in the first two. Continuing at the 50-month rate would result in an undepreciated value of $4,200; it is very likely that the vehicle will retain at least 40 percent of original value (and probably more), or $6,000. The adjustment upon sale will now skyrocket from $200 to $1,800. This would indicate that the vehicle has been depreciated $50 per month more than was necessary, over the 36 months of the service life. Reducing the monthly depreciation rate by this $50 to $250 would have the two positive benefits of improving cash flow and more closely match expense to the period of occurrence.

"Tax Refund"

Another problem that arises is what we might call the "tax refund" psychology of depreciation. Millions of taxpayers every year look forward with great anticipation to a fat check back from the IRS in the form of an income tax refund. They have permitted the government to withhold more money than they owe in taxes, and wait all year to get it back. Over-depreciation can have the same effect, not so much on fleet managers, but on branch and other field management. They are often willing to budget for higher lease payments (or depreciation charges) than necessary, and receive a large, lump sum credit when the resale proceeds exceed the undepreciated book value. Indeed, they often become dependent upon these credits, much in the way the taxpayer does with the tax refund. This is shortsighted and illogical. Prudent managers will see the value in paying less during their vehicles' time in service, and not receiving the large credit on resale. Doing so will accomplish two things; first, it will more closely recognize the depreciation expense in the period in which it occurs and, second, it will more than likely be cheaper on a net present value basis. Part of the difficulty in getting this message across comes from the use of the terms "gain" and "loss" on sale. These are, at the least, misleading terms to use to describe the accounting adjustment used upon the sale of a vehicle. Money is not "gained" or "lost"; there is merely an adjustment made on the books to rectify either over- or under-depreciation. Think of it, again, in terms of taxes. If a taxpayer receives a large refund, this is not because he is paying less in taxes; it is just because he has had too much withheld. In the same manner, having to send Uncle Sam a check isn't because more tax is being paid, it is because too little has been withheld.

Flexible Policy

The vehicle resale market, and thus actual depreciation experience, is varied and often unpredictable. How, in the face of this unpredictability, can a fleet manager avoid over-depreciating the company fleet? The first step is to capture and track actual depreciation. As vehicles are sold, the rate of depreciation experienced on the marketplace should be calculated, and compared with the rate of book depreciation used. This comparison should be done not only for each vehicle, but also for other vehicles of like type, as well as like mission (territory size, topography, mileage, etc.).

Next, it is important to have the flexibility to depreciate vehicles at the rate necessary to ensure a close match to actual experience. For leased fleets, a lessor willing to provide the fleet with whatever depreciation rate it needs; for owned fleets, an accounting department willing to do the same. Now, categories of vehicles can be established, not necessarily by make or model, but based solely upon depreciation experience. It isn't practical, of course, to depreciate vehicles on an individual basis, but general categories can be created, and, unless a particular vehicle's mission changes, it can be rated the same way whenever it is replaced.

Many fleets will tend to over-depreciate their vehicles if they have lengthened their replacement cycles without tracking actual depreciation, and making appropriate adjustments in their book depreciation rates. It is a relatively simple matter to do so, and the company will benefit from better cash flow, lower net present value cost, and a much clearer picture of vehicle expense

Originally posted on Automotive Fleet

More Fleet

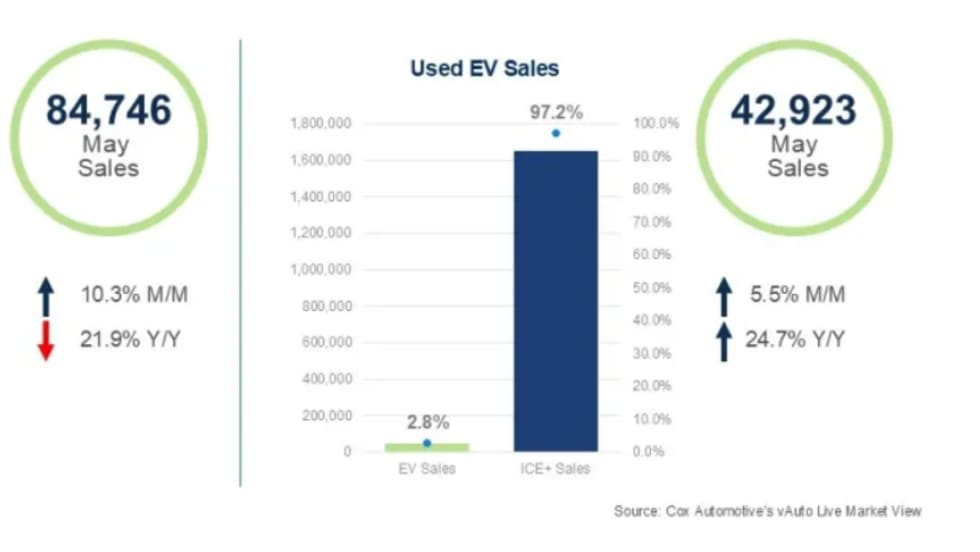

Used EVs Strengthen Overall Electric Vehicle Market

The latest sales data point to several reasons for the divergent trends in new and used EVs that can factor into fleet cycling decisions.

Read More →

Wholesale Used Vehicle Market Sustains Moderate Rise In Values, Prices

Trends continue to normalize after a strong start to the year, as consumers contend with higher gas prices in the coming summer months.

Read More →

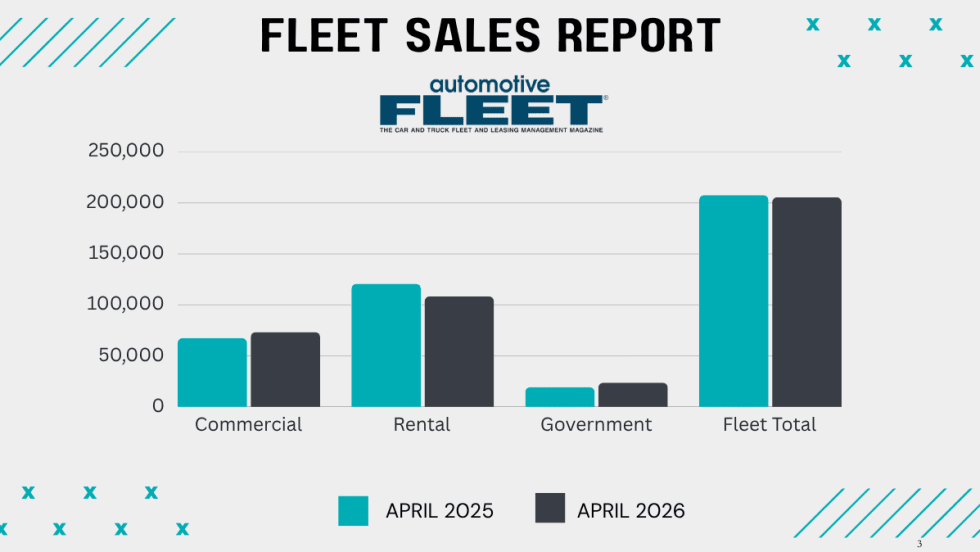

Commercial Fleet Sales Still Lead Sectors Despite May Mini Dip

The U.S. economy's continued growth and positive business investment are creating a favorable environment for fleet vehicle demand.

Read More →

The Data-Driven Haul: 5 Ways AI is Leveling the Playing Field in Auto Transport

Large and small transport fleets are becoming more competitive as predictive analytics and real-time data inform the logistics decision chain.

Read More →

How to Speak the Same Language on Fleet Safety

Drivers, supervisors, and data often speak different safety “languages.” Getting on the same page will drive better results.

Read More →

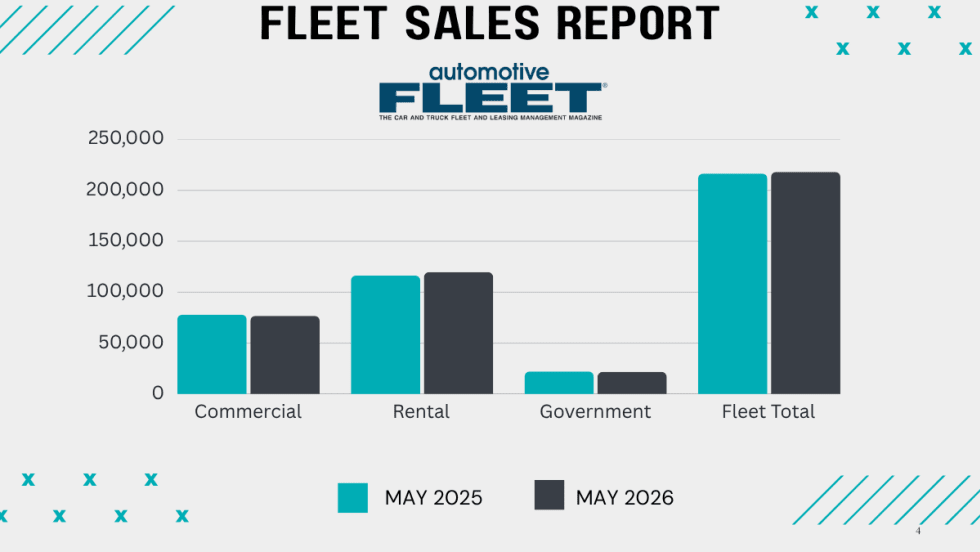

Commercial Fleet Sales Show Healthy Gains

So far, the fleet sector is outshining government and rental fleet sales this year as economic growth spurs more business investment.

Read More →

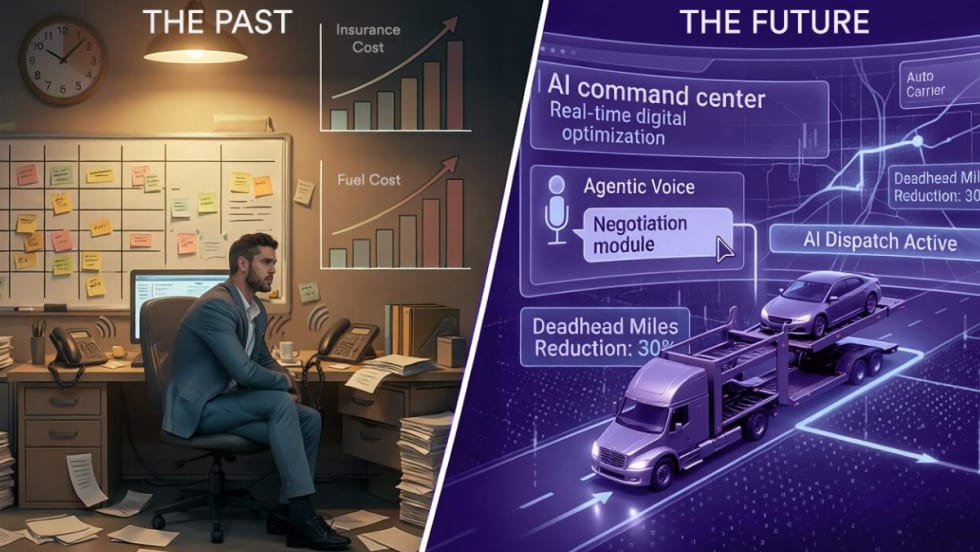

The Predictive Pivot: How AI and Data Are Redefining Auto Logistics in 2026

AI is no longer a luxury but the baseline for profitability in 2026. Auto haulers that adopt these tools now will quickly outpace those using manual workflows and taking a wait-and-see approach.

Read More →

The Predictive Pivot: How AI and Data Are Redefining Auto Logistics in 2026

AI is no longer a luxury but the baseline for profitability in 2026. Auto haulers that adopt these tools now will quickly outpace those that use manual workflows or take a wait-and-see approach.

Read More →

CAR 2026 Recap Part 2: Closing the Gap Between Data & Remarketing Value

The second half of CAR 2026 examined how fleets can translate lifecycle strategy, vehicle data, and market shifts into higher real-world results.

Read More →

CAR2026 in Two Words: Velocity, Value (Part 1)

The 2026 Conference of Automotive Remarketing convened with a mandate to involve a new constituency — fleet managers — and an updated mission to demonstrate unrealized value in de-fleeted vehicles.

Read More →