Related News:New Vehicle Supply Rose Despite UAW Strike

Vehicle Markets in Flux: How Are Fleets Doing?

The recent Fleet Forward Conference presented updates to the fleet, used vehicle, and electric vehicle supply and demand.

December 4, 2023

Tyson Jominy, vice president of data and analytics at JD Power, told conference attendees that most vehicle buying segments are trailing fleet since fleet operations are willing to pay top dollar for vehicles, which prompts the automakers to sell more into fleet and keep the retail prices high. He spoke Nov. 9, 2023 at the Fleet Forward Conference in Santa Clara, California.

Photo: Martin Romjue / Bobit

7 min to read

What's the bottom line on the current automotive market? Automakers are producing more vehicles, and as a result, selling more to everyone. The number of retail vehicle buyers is growing, but at a slower rate.

“So where are we right now? There's a lot of press, a lot of misinformation out there; half-truths, and in some cases lies,” said Tyson Jominy, vice president of data and analytics at JD Power, who keynoted Nov. 9 at the Fleet Forward Conference in Santa Clara, California. "In almost every one of my slides, the answer is always better than last year, but not quite to where we were in 2019.”

Supply Directed to Fleet Channels

On the fleet side, automakers are selling new vehicles directly to the fleet channels, such as daily rentals for government fleets and corporate fleet accounts, Jominy said. Fleets generate about a fifth of automotive industry business.

“It's growing dramatically, up 50% from a year ago. We’re almost back to where we were with fleet sales in 2019.”

The rest of the buying segments are trailing fleet since fleet operations are willing to pay top dollar for vehicles, which prompts the automakers to sell more into fleet and keep the retail prices high, Jominy said. Some automakers are reporting $17,000 increases in transaction prices compared to those of 2019.

Gone are the days when an oversupply of vehicles would be dumped into the fleet channel at discounts, he said. “Now, if we start to produce too many of a certain kind of vehicle, we have an equally profitable channel, which is the fleet channel,” he said.

Rebounding Up to a Point

Overall, vehicle supply and production have been rebounding from the pandemic era slowdowns, he said. Vehicle production is up to 15.6 million annually in the U.S. The industry lost about 7.5 million in vehicle sales since the start of COVID. Some of those losses result from fleets keeping vehicles longer, thereby forgoing or delaying replacement purchases. Meanwhile, retail consumers are waiting to buy vehicles, as in waiting for the right colors and the right prices/interest rates. So even if the industry wanted to get back to the 17.5 million in annual vehicle sales before COVID, it couldn’t because the demand in an atmosphere of high pricing pressures is not all there, Jominy said.

Of the vehicle model segments, smaller SUVs are growing the fastest since 2019. Since COVID started, 60% of all vehicle sales are SUVs, about 20% are cars, and another 20% are trucks. And while vehicle sales have shifted for years from sedans to SUVs, that trend is receding, except in the fleet segment.

“When I look at fleet sales, there's a very dramatic shift going on, and the shift away from cars toward SUVs is still happening,” Jominy said. “And I don't see that anywhere else in the industry. The way we came back both by automaker and by segment is radically different than where we were in 2019.”

Used Vehicle Supply to Remain Tight

On the used vehicle front, supply will remain tight for the next few years, keeping prices higher in the wholesale vehicle channels through mid-decade. Even when the total volume of used vehicles increases, the supply will not get back to pre-COVID levels due to fewer lease returns.

The backbone of the entire U.S. market — the three-year-old off lease vehicle — is not coming back to dealers at the same rate as before, reducing that supply line, Jominy said. “With a lower supply of used vehicles, on average, we will expect higher prices of used vehicles.”

While high used vehicle prices will at some point revert, they will only fall back to previous highs, and remain historically higher than prior averages, he said. He referred to the COVID-driven used vehicle price spike as a “Mt. Everest” on the price graph of the last few years.

Prices will come down, but they will ease and moderate out at a level to what would have been the best year in history, he said.

“Basically, we're talking about end of the decade until U.S. supply levels will reach pre COVID levels,” he said. “COVID will be a 10-year event in the used vehicle sector,” he added. “I've been in my job 14 years, and I'm still going to be talking about COVID almost to when I retire at this rate, because the U.S. market is still quite impacted by it and will not return to normal for several more years.”

EVs Turning Negative, But Numbers Still Positive

Electric vehicles have seen a spate of negative press with more potential buyers reluctant to pursue them. But the numbers still show a steep rise in EV purchases this year.

“Even as we've been talking about how nobody wants EVs and everyone hates them we’ve actually been selling a lot more EVs with the share of the industry hitting 9% on a retail basis in September,” Jominy said. Most sales still go to Tesla, which despite competition and price cutting, retains 60-62% of the new EV market.

Today there are 48 electric vehicle models on the ground, compared to 16 in 2019. Most are selling for between $50,000 and $60,000. In 2024, there will likely be 80 EV models on the market.

Despite such momentum, the average new car dealer in in the U.S. sells fewer than one EV per month, which causes days’ supply to reach the 100 level, hence the negativity, Jominy said.

EV-ICE Pricing Parity?

Determining price parity between EVs and ICE vehicles is near impossible given the varying levels of government and utility rebates, tax credits, incentives, and sales tax levels among the states for electric vehicles. “What does price parity even mean anymore?” Jominy asked. “An automaker can't see the price parity. Even if you're Tesla and you've got consistent prices for everybody, where you live causes radical differences in total ownership costs.”

Given the expected future demand for EVs, public charging will not be able to keep up, Jominy said.

“EVs may or may not be right for your fleets,” he said. “But something to keep in mind is there is very little (charging) infrastructure, at least from the federal government. In terms of how government is spending our money, it is highly skewed toward variable marketing and getting consumers into EVs and nothing for making EVs livable.”

Consumers need a “map” to figure out and understand the “Byzantine requirements” surrounding the purchase of vehicles, such as the income limits, pricing guidelines, and location of where the EV is built, Jominy said.

As a result, 55% of all EVs are being leased, since the benefit amounts to $3,500 for the lessee and avoids the tax forms, reporting requirements, and lower resale values brought on by the new EV price cuts.

Citing the EV index at JD Power, affordability in October 2023 hit 102% for EVs, which means that on average, an EV is 2% cheaper to own than an ICE vehicle for the first time ever, Jominy said. He credits the myriad federal, state, and local utility funds and credits that reduce the cost of owning an EV and even provide some chargers for free. Ownership costs still vary based on mileage and local area, but overall EVs can be a better purchase financially than an ICE vehicle, he said.

On the lack of reliable public charging stations, for example, Jominy underscored that 88% of all EV charging happens in homes. But now the growth in data will help EV owners identify in real time which public chargers are working, when they are available, and the speed of the charge.

“As you get into your fleet, you want to know if you can get these vehicles charged,” he said. “The good thing is that now the data is finally starting to pour in about public charging.”

Despite the negative press on EVs, J.D. Power stats show consumer consideration is still high as the data surrounding EVs expands and can help identify and solve problems. Data also helps a fleet operation figure out which fleet vehicles to replace with EVs, whom to assign them to, and where to deploy them.

“That's a very hyper local situation, depending on where you are, where your people are, and where your customers are, which can greatly impact your cost of ownership,” Jominy said. “It requires some sophisticated analysis.

“Now we’ve got a lot of great data out there that can help you solve some of these problems, like total cost of ownership and working through all the pieces of what goes into an electric fleet.”

Subscribe to Our Newsletter

More Fleet

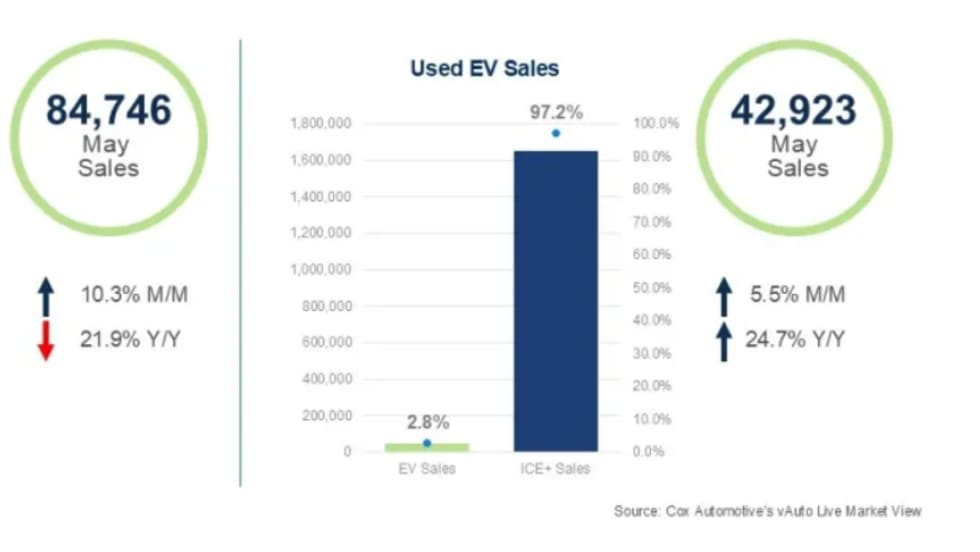

Used EVs Strengthen Overall Electric Vehicle Market

The latest sales data point to several reasons for the divergent trends in new and used EVs that can factor into fleet cycling decisions.

Read More →

Wholesale Used Vehicle Market Sustains Moderate Rise In Values, Prices

Trends continue to normalize after a strong start to the year, as consumers contend with higher gas prices in the coming summer months.

Read More →

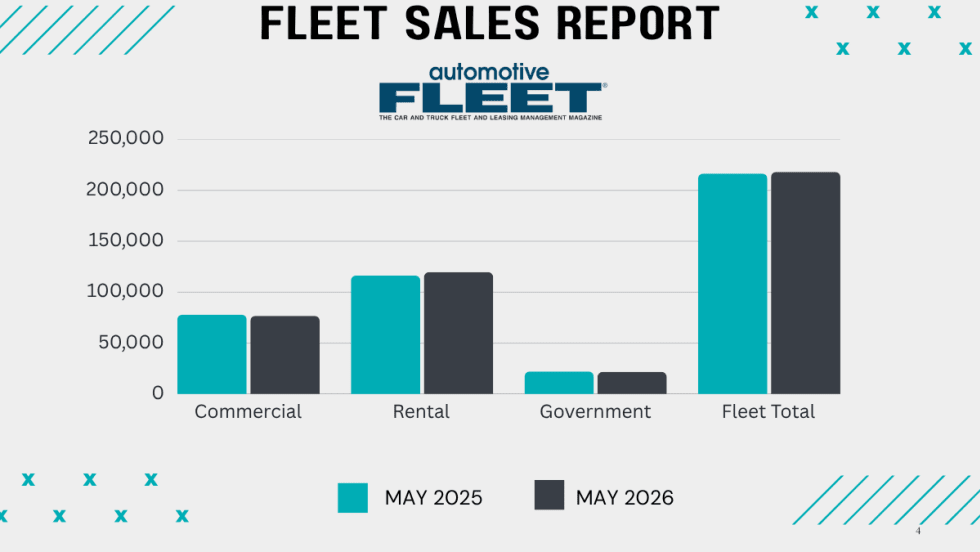

Commercial Fleet Sales Still Lead Sectors Despite May Mini Dip

The U.S. economy's continued growth and positive business investment are creating a favorable environment for fleet vehicle demand.

Read More →

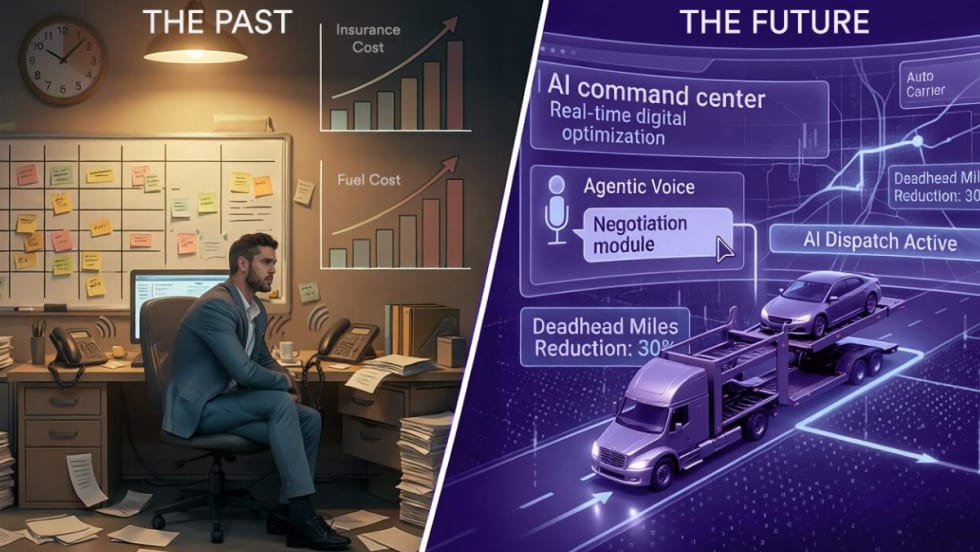

The Data-Driven Haul: 5 Ways AI is Leveling the Playing Field in Auto Transport

Large and small transport fleets are becoming more competitive as predictive analytics and real-time data inform the logistics decision chain.

Read More →

How to Speak the Same Language on Fleet Safety

Drivers, supervisors, and data often speak different safety “languages.” Getting on the same page will drive better results.

Read More →

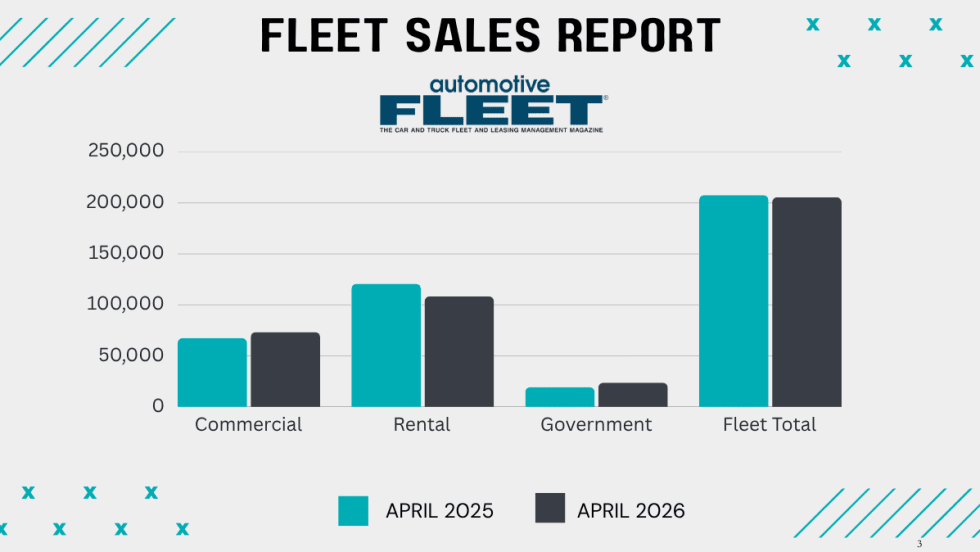

Commercial Fleet Sales Show Healthy Gains

So far, the fleet sector is outshining government and rental fleet sales this year as economic growth spurs more business investment.

Read More →

The Predictive Pivot: How AI and Data Are Redefining Auto Logistics in 2026

AI is no longer a luxury but the baseline for profitability in 2026. Auto haulers that adopt these tools now will quickly outpace those using manual workflows and taking a wait-and-see approach.

Read More →

The Predictive Pivot: How AI and Data Are Redefining Auto Logistics in 2026

AI is no longer a luxury but the baseline for profitability in 2026. Auto haulers that adopt these tools now will quickly outpace those that use manual workflows or take a wait-and-see approach.

Read More →

CAR 2026 Recap Part 2: Closing the Gap Between Data & Remarketing Value

The second half of CAR 2026 examined how fleets can translate lifecycle strategy, vehicle data, and market shifts into higher real-world results.

Read More →

CAR2026 in Two Words: Velocity, Value (Part 1)

The 2026 Conference of Automotive Remarketing convened with a mandate to involve a new constituency — fleet managers — and an updated mission to demonstrate unrealized value in de-fleeted vehicles.

Read More →