Close-Up:Making Money on EVs Just Got Harder

3 Headwinds That Will Batter the Auto Industry

Analysis: Slowing EV adoption, an expensive UAW labor contract, and higher consumer interest rates will diminish the profits and gains of recent years.

by Brian Finkelmeyer

November 30, 2023

Reluctant consumers remain concerned about EV charging infrastructure, range, and future resale values.

Photo: Bullet EV Charging Solutions

6 min to read

Catching trade winds is the fastest way for sailors to navigate across the ocean. Everyone loves it when the winds are at their back, but trouble can arise when the winds change, and they eventually do.

The auto industry has been sailing for the past three years with forceful tailwinds generated by COVID-induced economic stimulus and reduced vehicle production. Automakers and dealers alike have enjoyed turning their limited inventories quickly, huge margins, and soaring stock prices.

But as we approach the final weeks of 2023, with the global pandemic now solidly in our rearview mirror, the winds are clearly changing direction. Even Wall Street, which pumped up auto industry stocks during 2021 and 2022, is beginning to have a more tepid outlook for the industry. As we set sails for 2024, I believe three dynamics are creating new headwinds for the industry.

Electric vehicle (EV) adoption is happening much slower than expected, and the profit margins are abysmal.

The new UAW labor agreement will squeeze future profit margins for the Detroit 3 and has placed pressure on non-unionized plants in the South to increase wages.

The rising cost of borrowing money due to high interest rates is impacting consumers, dealers, and automakers alike.

Growing Concern about EV Demand and Margins

Two years ago, legacy car makers began placing big bets on EV development partly due to Wall Street’s infatuation with EV manufacturers like Tesla, who were rewarded with huge valuations. EV sales have continued to grow from 1% of total industry volume in 2019 to nearly 8% this year, according to estimates from Kelley Blue Book.

But the looming question on everyone’s mind is whether the market has reached peak demand for the current EV offerings. Cox Automotive’s latest inventory tracking shows EV days’ supply is near 100 days’ supply vs. 67 for the wider industry. Reluctant consumers remain concerned about charging infrastructure, range, and future resale values.

As a result of this sluggish demand, incentives continue to climb, reaching close to 10% of transaction price in September before retreating some in October, according to Kelley Blue Book. The comparable overall industry level remains below 5%. Tesla, the EV leader in the U.S. market by far, has been hyper-aggressive in dropping prices on their popular models by an average of $16,687 during the past 12 months. And those price cuts are pressuring the entire industry. Ford reported an EBITA loss of $1.3 billion in Q3 in its Model-e business, demonstrating how challenging this transition will be. And Mercedes Benz’s CFO recently commented, “I can hardly imagine the current status quo is fully sustainable for anybody.”

These shifting winds are causing OEMs to reshape their EV ambitions. GM announced it is abandoning its goal of producing 400,000 EVs by mid-2024. They are also postponing a $4 billion EV truck plant project in Michigan. Ford recently announced they are postponing $12 billion worth of planned EV investment due to “tremendous downward pressure on prices.” Honda just announced they are canceling their partnership with GM to produce a range of less expensive EVs. And lastly, VW just postponed their flagship Trinity EV plant development in Germany to 2030.

Jack Hollis, the head of sales at Toyota, said, “It took us 25 years, and we (the industry) are still not at 10% hybrid; the consumer is not demanding EVs at that level.” Toyota continues to advocate for a broad range of fuel types to meet environmental and consumer needs instead of solely focusing on EVs.

Bottom line: The EV transition is going to be a drag on the U.S. auto market for years to come.

Costly New UAW Labor Agreement

Last month, the UAW pulled off a historic victory for their members with wage increases upwards of 60% for new hires, and Ford CFO John Lawler said the new contract could add upwards of $850 to $900 of additional cost to every vehicle Ford produces.

Most interesting, the UAW only represents 140,000 of the 780,000+ auto workers in the U.S. (based on the Bureau of Labor Statistics). Over the years, the UAW made numerous unsuccessful attempts to unionize non-domestic auto plants in the South. With this massive haul for UAW workers, companies like Toyota, Honda, and Hyundai are already announcing pay increases for their manufacturing workers, and more companies are likely to follow to fend off future UAW unionized efforts at their plants.

Labor costs will rise for all automakers, regardless of the UAW’s union-drive efforts in the South. Wall Street is concerned that the automakers will be unable to pass this added labor cost onto consumers or find $900 worth of efficiencies to offset it. The net result will be lower margins moving forward. This issue creates another level of headache for the legacy OEMs building EVs because they lose a lot of money on each unit they sell.

Effects of Interest Rates on the Car Business

Cox Automotive reports that new-vehicle inventories were up 62% versus last year at the beginning of November. This, coupled with higher floor plan rates, has created downward financial pressure. One domestic dealer reported that his inventory holding expense had grown from $49,000 in 2022 to $670,000 in 2023, a 13x increase.

Vehicles are turning slower, the cost of carrying them is much higher, and I’m hearing about dealers turning down their monthly vehicle allocations, an unthinkable behavior 12 months ago. In the most recent quarterly Cox Automotive Dealer Sentiment Index survey, 61% of dealers said interest rates were the #1 issue holding their business back.

Consumers have also felt the pain of rising rates: new car payments increased almost 10% from last year, and 86% of that increase is attributed to higher rates. The average new car interest rate for consumers is now about 9%. In the fall of 2021, it was closer to 5.5%.

As some OEMs begin to feel softening demand, they are turning to “APR buy-downs” to spur retail sales. The incentive cost of buying the rate down from 9% to 3.99% is not cheap; imagine Hyundai’s expense of offering 0% for 60 months on select models. This situation is not likely to abate anytime soon and will continue to be a drag on automaker margins.

Still Hanging in With Higher Revenues

Despite concerns over the changing trade winds, the auto industry will finish 2023 far ahead of what was predicted. Cox Automotive (as well as many other forecasters) initially forecast a 14.1-million-unit market for 2023. The revised forecast calls for the industry to finish near 15.3 million units. General Motors recently reported their earnings could be as high as $10.9 billion, up from their initial estimate of $9.9 billion. AutoNation’s earnings per share improved from $4.97 in 2019 to $24.12 forecast for this year. Dealers and Automakers are continuing to print money despite the industry challenges.

The auto industry’s fundamentals remain extremely healthy. Despite challenges with EV adoption, higher labor costs, and higher interest expenses, as long as the automakers remain disciplined with production levels and closely align supply with demand, the industry is well positioned for smooth sailing for years to come.

Brian Finkelmeyer is the senior director of new car solutions at Cox Automotive.

Subscribe to Our Newsletter

More Operations

Stop Remarketing Electric Vehicles Like Gas Cars

The advantages and attributes of electric vehicles are upending the traditional remarketing cycle, requiring fleet sellers to rely on new factors and approaches detailed below.

Read More →

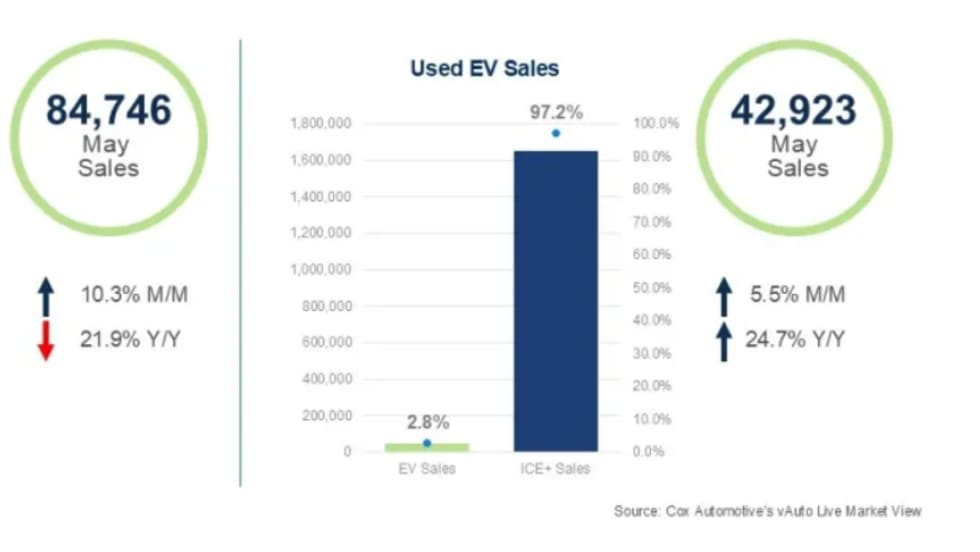

Used EVs Strengthen Overall Electric Vehicle Market

The latest sales data point to several reasons for the divergent trends in new and used EVs that can factor into fleet cycling decisions.

Read More →

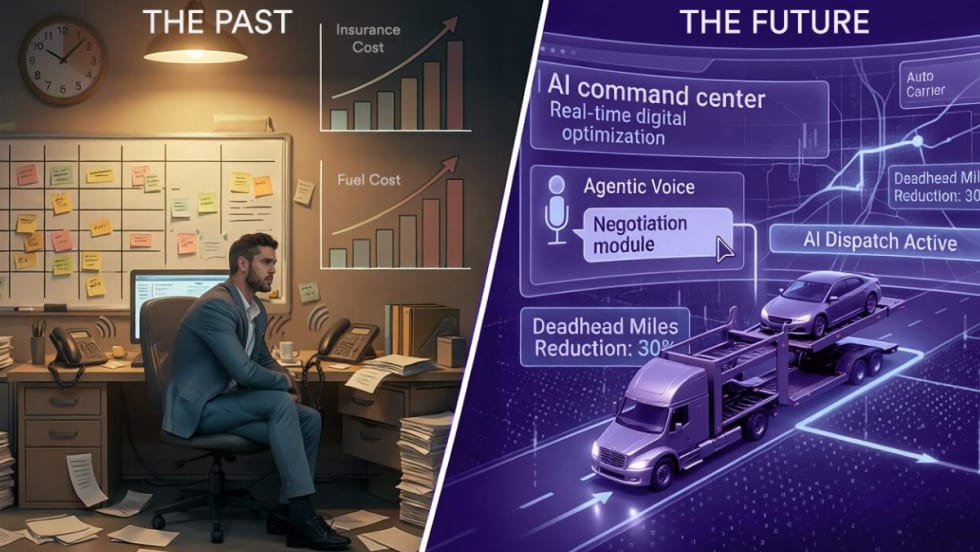

The Data-Driven Haul: 5 Ways AI is Leveling the Playing Field in Auto Transport

Large and small transport fleets are becoming more competitive as predictive analytics and real-time data inform the logistics decision chain.

Read More →

How to Speak the Same Language on Fleet Safety

Drivers, supervisors, and data often speak different safety “languages.” Getting on the same page will drive better results.

Read More →

2026 CAR Awards Celebrate Industry Excellence

CAR’s annual Fleet Remarketing Awards opened a reimagined 2026 conference designed to bridge the worlds of fleet management and automotive remarketing.

Read More →

The Predictive Pivot: How AI and Data Are Redefining Auto Logistics in 2026

AI is no longer a luxury but the baseline for profitability in 2026. Auto haulers that adopt these tools now will quickly outpace those using manual workflows and taking a wait-and-see approach.

Read More →

The Predictive Pivot: How AI and Data Are Redefining Auto Logistics in 2026

AI is no longer a luxury but the baseline for profitability in 2026. Auto haulers that adopt these tools now will quickly outpace those that use manual workflows or take a wait-and-see approach.

Read More →

CAR 2026 Recap Part 2: Closing the Gap Between Data & Remarketing Value

The second half of CAR 2026 examined how fleets can translate lifecycle strategy, vehicle data, and market shifts into higher real-world results.

Read More →

CAR2026 in Two Words: Velocity, Value (Part 1)

The 2026 Conference of Automotive Remarketing convened with a mandate to involve a new constituency — fleet managers — and an updated mission to demonstrate unrealized value in de-fleeted vehicles.

Read More →

CAR 2026: Get the Wall Street Update on the Key Players in Remarketing

From a Wall Street analyst's take on remarketing's key players to whether fleets need their own version of Carfax, CAR 2026's afternoon roundtables will answer key operational and industry questions.

Read More →