The AutoIMS Industry View is a compendium of metrics featured in the AutoIMS Sales Scorecard that reflects the entire AutoIMS database — most of the commercial sales volume at wholesale auto auctions in North America. The complete report is available at AutoIMS

AutoIMS 2Q Report Shows Leaps in Converstion Rate, Sale Prices

The company's second quarterly report in a row highlights key aggregate metrics for the auction industry.

August 10, 2021

AutoIMS uses an array of superheroes to promote its quarterly Industry View report.

Graphic: AutoIMS

3 min to read

With two quarters of data accumulated, AutoIMs is gaining more clarity about key industry remarketing and auction trends, according to its latest quarterly report released Aug. 9. One defining mega-trend is low vehicle volume for the foreseeable future.

Among notable increases in the AutoIMS Industry View:

The conversion rate, or percentage of vehicles sold on a day in which they were offered, rose to 72% in the second quarter compared to 58% in 2Q 2020.

The average vehicle sale price was $16,096.20 in the second quarter, compared to $13,089.76 in 2Q 2020.

The average mileage hit 83,546 miles in the second quarter, compared to 71,982 in 2Q 2020.

Major year-over-year differences are beginning to appear, reflecting the unique supply chain challenges faced by the industry alongside the continuing economic recovery.

In addition to the microchip shortage and supply chain issues, the auction industry is seeing a carry over side effect of previous (pre-pandemic) decisions on how many vehicles to make of certain types, said Joe Miller, vice president of client experience at AutoIMS. "Their manufactuing mix is affecting their ability to deliver what consumers want today. New cars ripple out to the used car market and that drives values and demands on used cars," he said.

Three other reasons auctions are seeing lower vehicle volume is rental cars staying in fleets longers, more leased vehicles being bought by the lessor instead of shipped to the wholesale market, and more vehicles sold upstream of auctions, Miller said.

Based on his conversations with AutoIMS clients, Miller said the volume squeeze will remain for about another years, turning up in the second half 2022 and adjusting back to normal levels of a few years ago in 2023.

In the latest report, AutoIMS user activity leveled off after peaking in March 2021, although June saw the biggest number of new users entering the system this year. Key clients continue to use this time of lower volume to focus on projects including workflow enhancements, integration updates, scorecard revisions, system conversions, and more, laying the groundwork for more efficiency when volumes bounce back

Insights on the Repossession Market

Using the Sales Scorecard, Auto IMS analyzed a cross-section of large auto lenders, focusing on the limited repossession volume it saw in the first half of the year.

Here are some key findings from that market segment with comparisons to the entire database (all segments, as captured in the remainder of the Industry View):

Average sale price: $9,185, almost $6,000 less than the overall average

Average mileage: 104,705, more than 20,000 miles higher than the overall average

Average model year: 2013.9, a full year older than the full sample.

Average auction charges: $366, about $22 less spent per unit than the overall.

Average days to sell: 43.7,16.5 days longer sale cycle than the overall average.

Damage estimate (non-salvage volume): $2,768, 58% higher than the overall average.

Average vehicle grade (non-salvage volume): 2.6

Conversion rate: 79.8% Higher than the overall average by nearly eight points.

If conversion rate is any indication, demand is high for the older, less-expensive repo segment. It stands to reason that with more involved CRs, fewer of these cars are selling in online-only channels, leading to a longer stay at auction.

Miller also attributed lower repossession supply to lenders that have adopted self-imposed curbs and leniency for borrowers, legally imposed moratoriums on repossessions, and fewer vehicles coming back to market.

More Auctions

Manheim Index Shows Used-Vehicle Wholesale Prices Up 2.1% in June

The market is seeing stronger appreciation in older used vehicles this year, and the most affordable segments have been among the year’s best performers.

Read More →

Stop Remarketing Electric Vehicles Like Gas Cars

The advantages and attributes of electric vehicles are upending the traditional remarketing cycle, requiring fleet sellers to rely on new factors and approaches detailed below.

Read More →

Used Vehicle Prices Climb Higher As Sales Pace Slows

The higher prices at used retail reflect strong wholesale values earlier in the spring, particularly for older, more affordable vehicles.

Read More →

Wholesale Used Vehicle Market Sustains Moderate Rise In Values, Prices

Trends continue to normalize after a strong start to the year, as consumers contend with higher gas prices in the coming summer months.

Read More →

Wholesale Used Vehicle Prices Slightly Up In April

The Iranian conflict and rising gas prices inject much uncertainty into the future wholesale used vehicle markets, as higher gas prices soak up spendable income from vehicle buyers.

Read More →

CAR2026 in Two Words: Velocity, Value (Part 1)

The 2026 Conference of Automotive Remarketing convened with a mandate to involve a new constituency — fleet managers — and an updated mission to demonstrate unrealized value in de-fleeted vehicles.

Read More →

CAR 2026 Session to Uncover the Missing Data That's Costing Fleets at Disposal

Work trucks lose value at remarketing, not because they aren't worth more, but because the data to prove it rarely makes it to the auction.

Read More →

TSD Mobility, UVeye Partner On Automated Vehicle Inspections

The enhanced technology allows rental car operations, dealerships, and auctions to compare a vehicle’s condition at pickup and drop-off within the same rental or loaner record.

Read More →

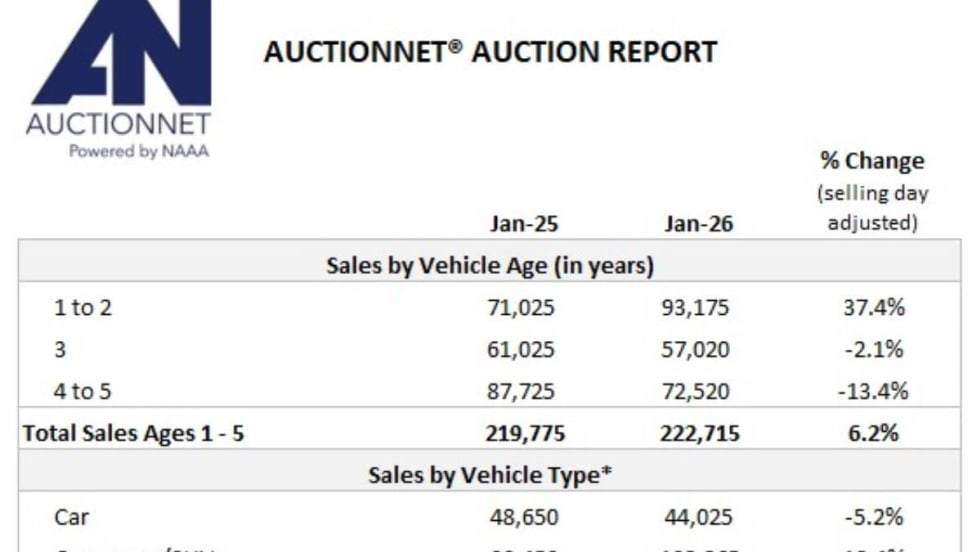

Auction Sales Kick Off 2026 In High Step

Winter snowstorms and frosty freeze-overs could not slow down the hot vehicle auction action nationwide in January.

Read More →

Plug Raises Capital To Grow Its Used EV Marketplace

The $20 million in Series A funding from Lightspeed will enable Plug to boost supply, develop more technology, and widen wholesale and retail sales channels.

Read More →