Background Article: IARA Leads on Consignor and Remarketer Compliance

Government ‘Rulapalooza’ Ready to Roll Out

Auto finance companies and remarketers should prepare to navigate a more active regulatory environment this year from the CFPB and FTC.

January 20, 2023

The Consumer Finance Protection Bureau and Federal Trade Commission are working together on all cylinders toward a common goal for consumer protection, like a perfect storm, according to an IARA compliance presentation.

Image: Bobit

7 min to read

As if economic and auto market headwinds weren’t enough, the financial side of the remarketing industry should prepare for a perfect storm of regulatory cooperation among two key federal agencies.

Recent actions and proposals from the Consumer Financial Protection Bureau (CFPB) and the Federal Trade Commission (FTC) could affect auto finance companies for consignors that need to closely track them and stand up for their interests, said Eric Johnson, a partner in the Oklahoma City office of Hudson Cook, who led an online session Jan. 13 hosted by the Education and Compliance Committee of the International Automotive Remarketers Alliance.

Johnson works with national and state banks, motor vehicle dealers, and automotive finance companies to develop and maintain nationwide consumer auto finance programs, online motor vehicle sales and assistance programs, litigation funding programs, and electronic payment programs.

Johnson referred to the current state of regulations as “Rulapalooza” because the agencies are issuing so many rules. The CFPB and FTC are positioned to work in lockstep to prop each other up and build on each other’s agendas, he said.

“The election did not deter them in the least. The CFPB and FTC are coming out full bore with many new rules.”

D.C. Political Shift May Only Go So Far

Johnson provided an overview of the Washington, D.C. political climate taking shape in the wake of a much smaller red wave than expected, with the Republicans garnering only a four-seat majority in the House of Representatives.

“All predictions are off,” Johnson said. “We might see a lot of battles in D.C. this year and not a lot of agreement in the House and Senate.”

In late 2021 and in 2022 before the elections, Rohit Chopra, director of the Consumer Financial Protection Bureau, outlined the focus of the agency: The CFPB plans to keep a close eye on competition; sharpen its efforts on repeat offenders of federal/agency orders; and restore the relationship in big banking tech and data. They also plan to prosecute or cite officers and executives of companies.

“They mean what they say when they will go after executives if they played a role in a violation,” Johnson said. “They’re not only going after the institution, but present and former executives with no immunity.”

Johnson warned that the CFPB is undeterred by election results, citing an example of a national bank that paid $2 billion in consumer redress and $1.7 billion in penalties. The bank was accused of unlawfully repossessing vehicles, denying mortgage modifications, bad bundling of financial products, and charging surprise overdraft fees.

The CFPB’s current approach draws opposing reactions from the two political parties, with praise from Democrats and criticism from House Republicans who plan more oversight through the House Financial Services Committee of what they consider an “unaccountable CFPB,” Johnson said.

In one example, House Republicans sent Chopra 10 questions and received only a one page response to them. They now contend Chopra and the bureau are not being transparent and circumventing the public comment process.

Eric Johnson, a partner in the Oklahoma City office of Hudson Cook, led a CFPB and FTC compliance session for members of the International Automotive Remarketers Alliance on Jan. 13, 2023.

Photo: Hudson Cook

CFPB Faces a Big Question

Despite a more aggressive stance, the CFPB could potentially lose its funding source, depending on the outcome of a lawsuit.

Instead of subjecting the CFPB to the annual appropriations process, in which agency funding can vary depending on which party holds power, Congress funded the new agency through the Federal Reserve. Because the Federal Reserve is self-funded, the law ensured that the CFPB has a consistent source of revenue, according to a report in The Regulatory Review.

On Oct. 19, 2022, the U.S. Court of Appeals for the Fifth Circuit held that the CFPB’s funding mechanism is unconstitutional, the Review reported. “On its face, the court’s decision is relatively narrow, only striking down a single agency rule regulating payday lenders. But the implications of the court’s decision stretch far beyond this one CFPB rule,” according to legal experts cited by The Regulatory Review. “If upheld on appeal, the decision could reshape the federal government’s ability to regulate financial markets and protect consumers from fraudulent activity.”

The case is now headed to the Supreme Court, where the stakes are high, according to a report by UNIDO US. “And the opinion already is casting a long shadow. Although every other court has denied this type of claim, companies facing penalties are now invoking the decision as a defense in enforcement cases covering a range of anti-consumer behavior,” according to the report.

“If given enough time, the Supremes could rule the funding mechanism is unconstitutional and that could cause chaos in multiple industries,” Johnson said. “It will drive the need for Congress to come up with a solution.” It could make the CFPB subject to appropriations.

The case has prompted many businesses that are subject to litigation from the CFPB to file legal briefs citing the 5th Circuit ruling as rationale for CFPB actions to be stayed pending the outcome of a final decision. As a result, many bureau actions are on hold.

“We’re watching the case in earnest to see what will happen,” he said. “The industry wants to get this resolved as soon as possible. If the funding is ruled unconstitutional, are they a valid agency? What rules are valid and which ones do you play by? Do you wind up back to day 1? What about all these fines and consent orders agreed to?”

Keeping an Eye on New Rules

Johnson advised auto finance companies should look at the following CFPB proposals that deserve public comment from the industry:

Registry of repeat offenders: This would collect and require non-bank financial firms to register with the bureau if they are subject to a consumer protection agency local or state order. Johnson called it “a public shaming list” that would invite repeated scrutiny. Firms would also need to register if under a consent order from a state or the federal government. “This puts a target on auto finance companies or non-bank financial firms to register themselves with a central repository,” he said, which would alert state attorney’s generals, regulators and plaintiff attorneys.

Non-bank reporting of arbitration clauses and contractual firms: If a non-bank entity has consumer contracts or terms, they too would have to register contracts with the CFPB. It targets non-bank or auto finance companies by requiring them to register those contracts, which may cause companies to look more closely at contracts, conditions and terms. They may scale those back knowing that regulators and plaintiff attorneys may see those on registries.

Both rules are open for public comments within the next few months.

FTC Dovetails with CFPB Efforts

The FTC is a political body that before the election consisted of three Democratic appointees and two Republican ones, but since one Republican resigned the commission tilts 3-1 with Lina M. Kahn as chair, Johnson said.

That means the FTC in 2023 will likely take a more aggressive approach in policing auto dealerships, trying to push unfair and deceptive practices rules on dealers, Johnson said. “The FTC has been really busy on their Rulapalooza going into 2023. They will be undeterred by what happened during the elections.”

Safeguards Rule Expands

The FTC has amended the proposed Motor Vehicle Dealers Trade Regulation Rule, which would do the following:

Prohibit motor vehicle dealers from making certain misrepresentations while selling, leasing, or arranging financing for motor vehicles.

Require accurate pricing disclosures in dealers’ advertising and sales discussions.

Require dealers to obtain consumers’ expressed informed consent for charges.

Prohibit the sale of any add-on product or service that confers no benefit to the consumer.

Require dealers to keep records of advertisements and customer transactions.

The rule, which has drawn 11,000 comments and counting, would be effective in June.

“We would see them go after dealerships for violations of the safeguards rule and see more enforcement of that,” Johnson said. “They could extend the deadline beyond June, but it’s unlikely given how aggressive they are with rules and enforcement actions. The six-month window has given people some breathing room, but we don’t see FTC taken the foot off peoples’ throats.”

Johnson said the FTC is supposed to consider all comments for revised final rules. The industry could file suit against the FTC to block the rule from becoming effective.

What Fees Are Junk?

The FTC’s pursuit of junk fees rules is extremely broad in affecting auto finance companies that charge any sort of convenience fee that could be classified as junk fees. “If you look closely at this rule, it could disrupt the entire economy,” Johnson said.

With Chopra and Kahn, the agencies are working together on all cylinders toward a common goal for consumer protection, like “a perfect storm,” which is unusually intense for two federal regulatory bodies.

The CFPB could also team up with state regulators to pursue auto finance companies. More “marvel team-ups” of State Attorney General offices and the CFPB also could emerge, drawing on the agency’s $780 million budget.

“We have not seen in our lifetimes the CFPB and FTC working in lockstep like they are now,” Johnson said. “You have the older brother FTC and the younger brother CFPB.”

Subscribe to Our Newsletter

More Banks and Credit Unions

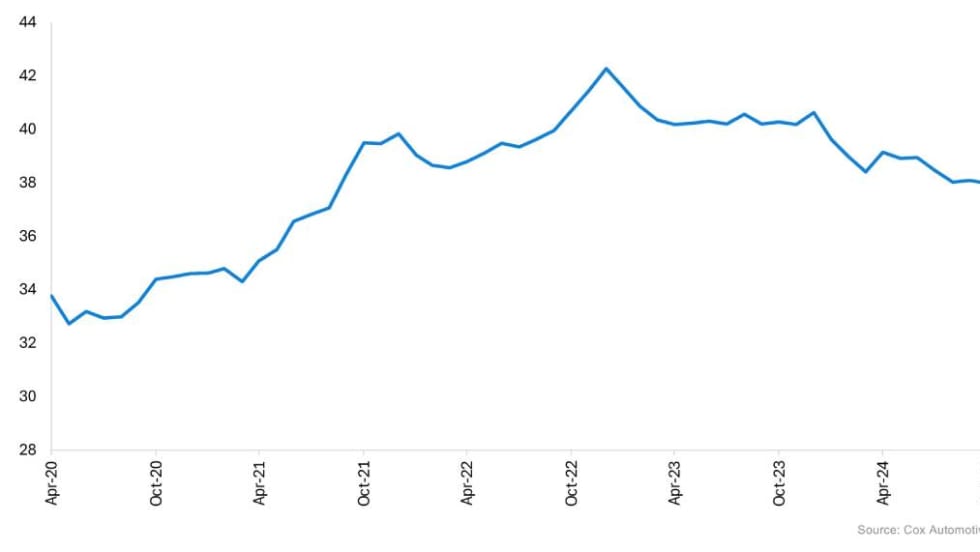

Tariff Burden Making New Vehicles Less Affordable

New-vehicle affordability declined in April to the worst level yet this year as the bite of higher prices and lower incentives reversed an improving trend.

Read More →

Strategic Remarketing Solutions Integrates with MeridianLink

The arrangement accesses cloud-based software designed to help financial institutions keep track of their vehicle and asset collections and limit repetitive clunky tasks.

Read More →

Why Business Groups Must Engage with Government

CAR 2023: Politics may be tough territory, but trade groups that build bridges in Washington, D.C. are less likely to get eaten at the regulatory table.

Read More →

Used Vehicles Accounting for Larger Share of Auto Finance Market

Used financing increased 2.4% year-over-year and reached 55.15% in the third quarter of 2019.

Read More →

Frontier Leads Early Wave of Lease Price Drops

Several manufacturers offered attractive discounts and competitive pricing on compact cars and SUVs, while most luxury and full-size vehicle brands maintained their lease prices.

Read More →

Fed Triggers Third Interest Rate Cut of 2019

The Federal Reserve announced a quarter-point interest rate reduction yesterday, its third such move this year. The target federal funds rate now stand at 1.5% after starting the year at 2.25%.

Read More →

Auto Loans Likely Won't be Affected by Recent Interest Rate Cut

Cox Automotive’s chief economist, Jonathan Smoke, said he didn’t expect the Fed’s latest move to match the impact of the July cut for auto manufacturers or dealers.

Read More →

Lease Credit Approval Rates Rise to 69.1% in July

Swapalease.com, a car lease marketplace, reports car lease credit applicants registered a 69.1% approval rate in July, a rise from the June rate of 65%.

Read More →

Fed Announces First Rate Cut in 11 Years

Federal Reserve Chairman Jerome Powell officially announced a widely expected cut to the federal funds rate yesterday, dropping the central bank's target by a quarter-point to 2%.

Read More →Credit Approvals Dip to 65% in Secondary Lease Market

Swapalease credit approvals registered 65% entering July, a drop from the 72.4% approval rate registered in May, the company announced.

Read More →